")

")

")

A Quick Take On TPG

TPG Inc. (NASDAQ:TPG) is an alternative asset manager for global institutional investors and individuals with a high net worth.

The firm is adjusting to a more challenging fundraising environment, but management believes it is well-suited to the current business climate.

Based on the performance of TPG Inc. stock in the past 12 months, I’m not convinced, so I’m Neutral [Hold] on the stock for the near term until we gain greater clarity on the direction for cost of capital, the close of its Angelo Gordon acquisition, and its fundraising results.

TPG Overview And Market

Fort Worth, Texas-based TPG invests client funds in alternative assets and seeks to generate superior risk adjusted returns.

The firm is led by Chief Executive Officer Jon Winkelried, who has been a board member since the company’s inception and has been CEO since 2021.

The company’s main offerings include:

-

Private Markets

-

Public Markets

-

Impact Funds

-

Real Estate

-

Other.

According to a 2021 market research report by Mordor Intelligence, the worldwide market for private equity deals is expected to grow at a CAGR (Compound Annual Growth Rate) of 11% from 2016 to 2026.

The main reason for this expected growth is growth in company buyout activity that depends on strategic relationships between corporates and private equity advisors.

Major competitive or other industry participants include:

-

Blackstone

-

KKR

-

The Carlyle Group

-

Providence Equity Partners

-

Advent International

-

Apollo Global

-

Others.

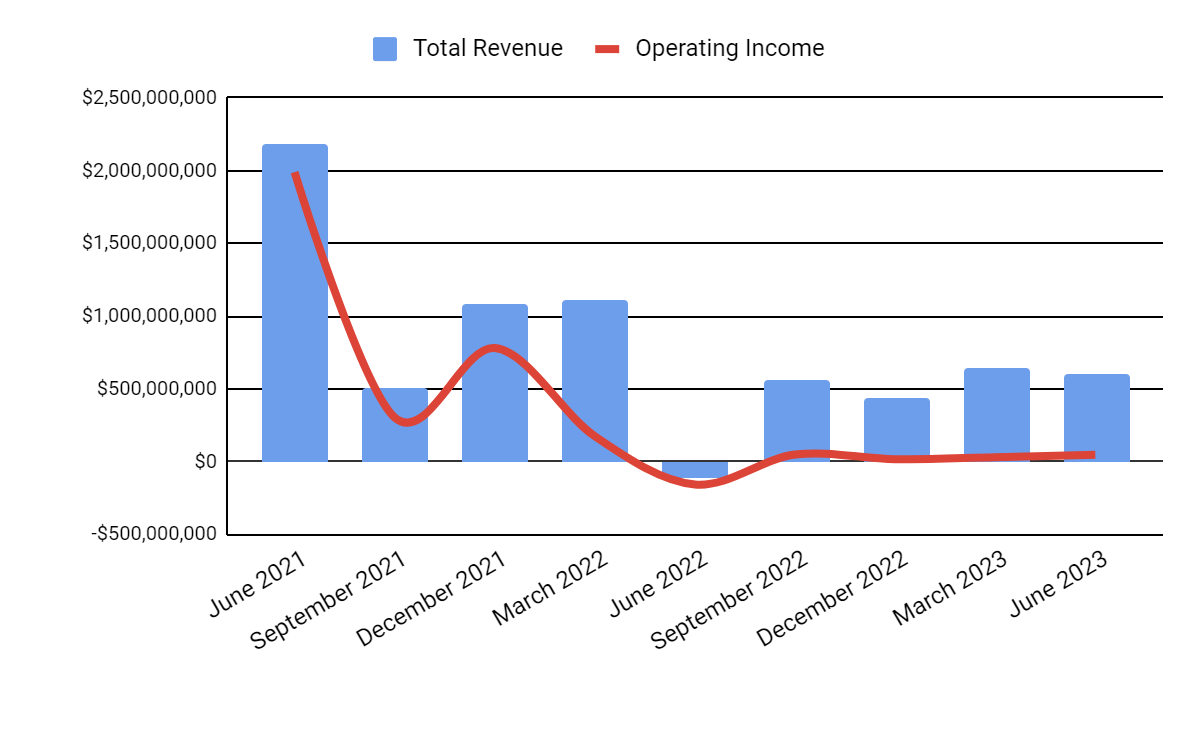

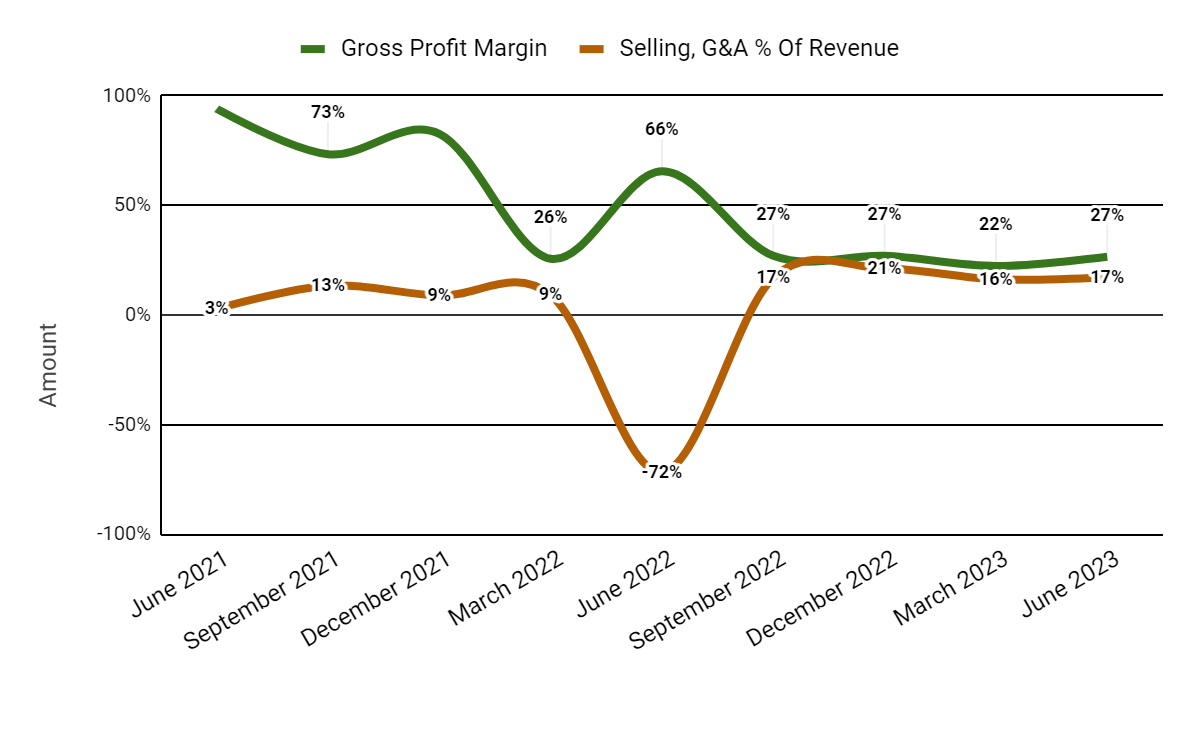

TPG’s Recent Financial Trends

Total revenue by quarter has dropped from highs during 2021; Operating income by quarter has also dropped sharply from 2021, although it has risen sequentially more recently:

Seeking Alpha

Gross profit margin by quarter has stabilized in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter have also flattened more recently.

Seeking Alpha

(All data in the above charts is GAAP.)

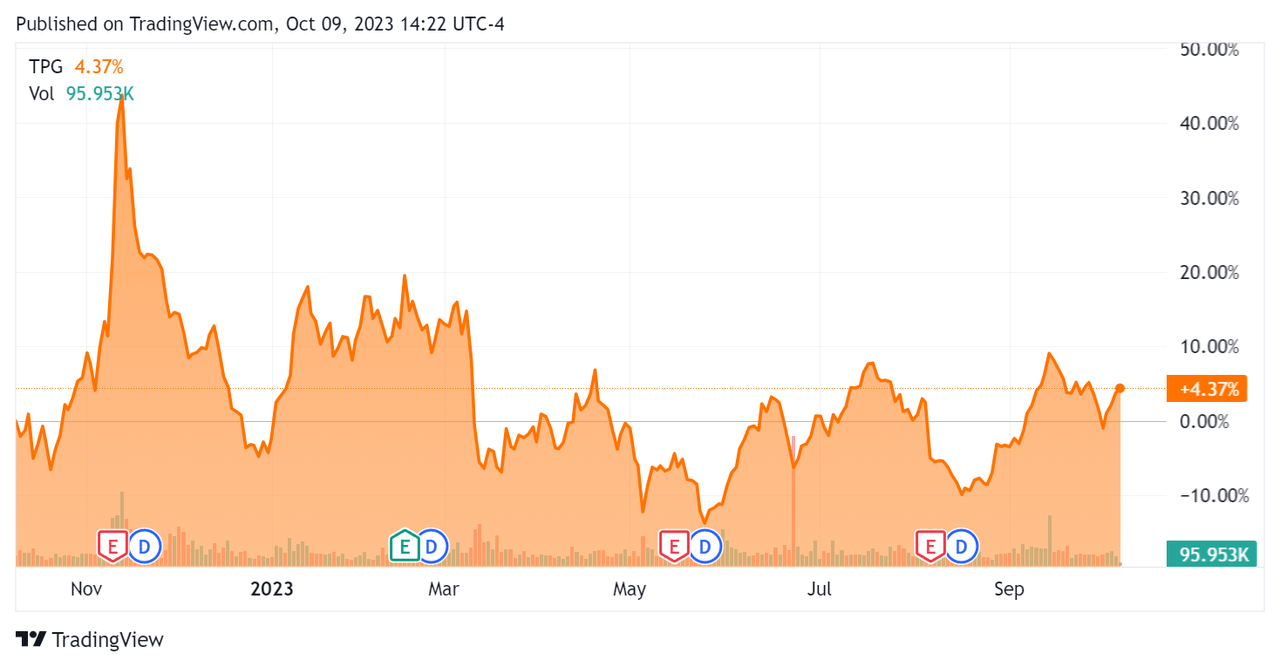

In the past 12 months, TPG’s stock price has risen only 4.37%:

Seeking Alpha

For balance sheet results, the firm ended the quarter with $897.6 million in cash and equivalents and $444.9 million in long-term debt.

Over the trailing twelve months, free cash flow was $1.2 billion, during which capital expenditures were $5.3 million. The company paid $1.194 billion in stock-based compensation in the last four quarters.

Valuation And Other Metrics For TPG

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

2.1 |

|

Enterprise Value / EBITDA |

26.7 |

|

Price / Sales |

1.1 |

|

Revenue Growth Rate |

-13.4% |

|

Net Income Margin |

5.8% |

|

EBITDA % |

7.9% |

|

Market Capitalization |

$9,330,000,000 |

|

Enterprise Value |

$4,720,000,000 |

|

Operating Cash Flow |

$1,210,000,000 |

|

Earnings Per Share (Fully Diluted) |

$0.00 |

|

Free Cash Flow Per Share |

$15.15 |

(Source – Seeking Alpha.)

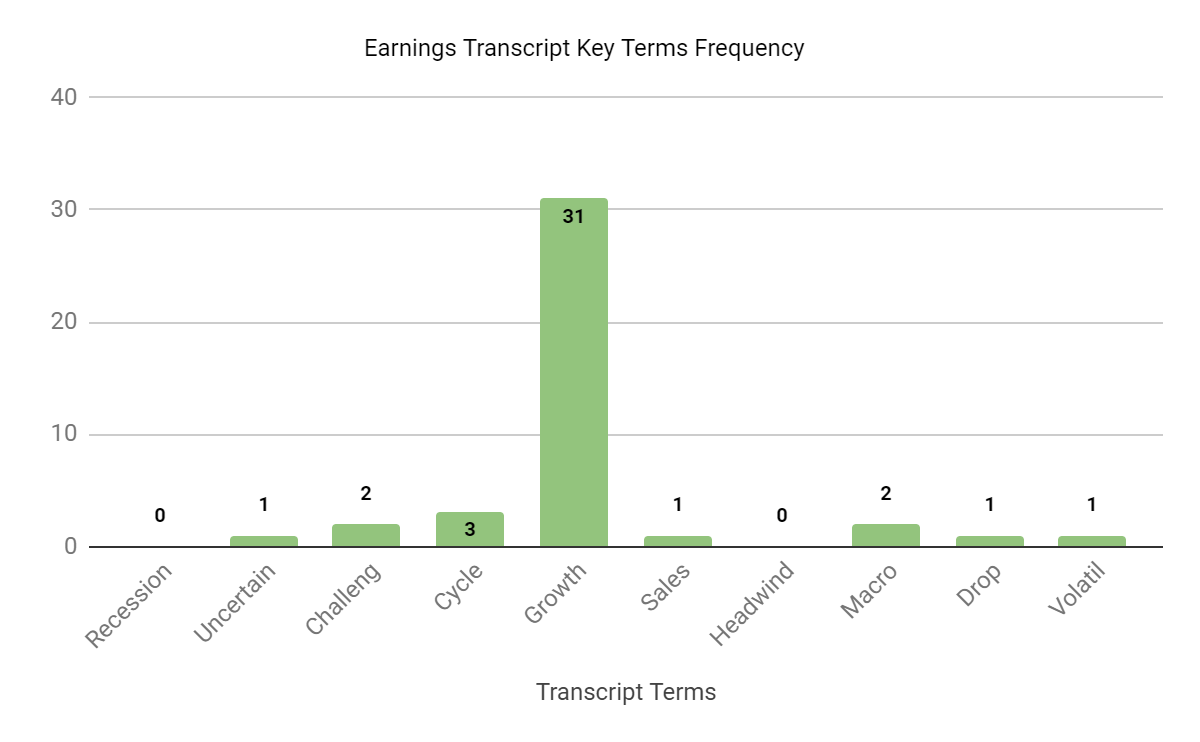

Sentiment Analysis

The chart below shows the frequency of certain keywords in the most recent management earnings conference call.

Seeking Alpha

The chart indicates the company is experiencing a challenging environment for fundraising but that the market volatility has been belied by reduced bid-ask spreads between buyers and sellers.

Analysts asked leadership about its fundraising progress and the pace of exits from capital deployments.

Management responded that the firm has longstanding relationships with investors and expects to raise the remaining $4 billion to $5 billion for the flagship funds.

Exit pace will increase due to faster progress on company transformations and greater strategic buyer interest. Management is focused on building portfolio value in the current environment.

Commentary On TPG

In its last earnings call (Source – Seeking Alpha), covering Q2 2023’s results, management’s prepared remarks highlighted the faster pace of transaction pipelines.

Also, corporates have “become significantly more active in restructuring their portfolios, pursuing acquisitions and divesting certain assets.”

These conditions present greater opportunities to deploy capital, either new investments or enhancing growth value creation for existing portfolio companies.

Total revenue for Q2 2023 fell sequentially but remained above $500 million, while operating income was $47.5 million.

Looking ahead, management believes that its “style” of private equity investing, that of transforming high-quality companies and accelerating growth, is well suited to the current market environment.

However, with the sharp rise in the cost of capital and the potential for a “higher-for-longer” rate environment, private equity firm stocks have diverged in their performance from the broader market.

With the acquisition of Angelo Gordon, TPG will gain entry into the credit investing business.

Direct lending is a hot business right now as banks pull back from the market in certain respects, so the acquisition will expand TPG’s offerings at a propitious time.

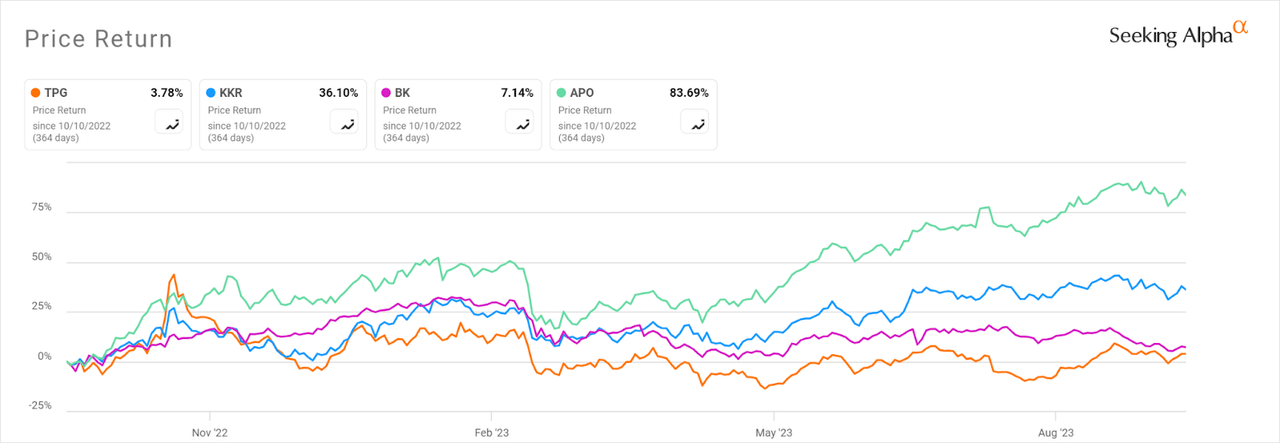

In the past twelve months, TPG’s stock price growth has underperformed a number of alternative asset manager stocks, as the chart from Seeking Alpha shows below:

Seeking Alpha

A big question is which direction the cost of capital environment will take in the coming quarters.

At least the company is seeing a reduction in bid-ask spreads, which may be a function of a more stable interest rate environment, enabling acquirers to better price acquisitions.

Until we gain further clarity on the outlook for the cost of capital, and the firm closes on and integrates its Angelo Gordon acquisition, I’m Neutral [Hold] on TPG Inc.

Read the full article here

")

")

2026-04-06")

")

")