")

")

One of the more interesting names to watch this year in the electric vehicle space has been NIO (NYSE:NIO). The Chinese player was looking to dramatically increase its sales thanks to refreshed models and new factory capacity coming online. Over the weekend, the company announced its Q3 delivery figures, and while the number was a new record as expected, I can’t recommend buying the stock just yet.

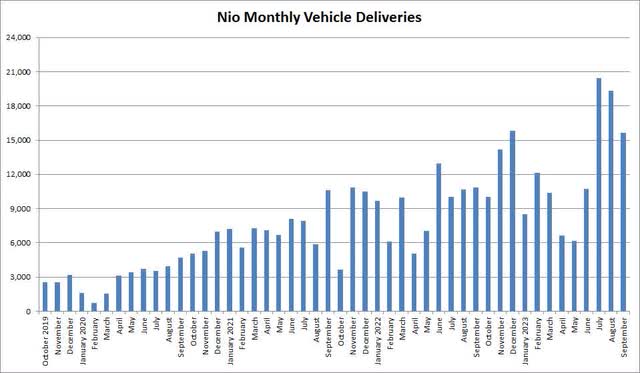

For the third quarter, NIO came in at 55,432 deliveries. This number was far better than any other period in the company’s history, and the figure turned out to be almost 900 units more than the first two quarters of this year combined. During Q3, NIO posted three of its four best monthly delivery numbers in its history. As the chart below shows, the company is doing a lot better now than it has been in the past couple of years.

NIO Monthly Deliveries (Company Website)

Unfortunately, I do have to throw some cold water on this quarterly result. First, management had guided to a range of 55,000 to 57,000 vehicles for Q3, so NIO did miss the midpoint by more than 565 vehicles. Given that this delivery forecast was given in the last few days of August, this implies that September was a bit softer than expected. In total, this puts the company at just under 110,000 vehicles for the first nine months of the year.

Management’s yearly goal for 2023 was for about 245,000 deliveries, so it appears NIO will fall well short of that. This isn’t the first time that yearly deliveries will come in well below expectations. In previous years, the coronavirus did hurt results, but NIO also had supplier issues and multiple factory shutdowns for upgrades. The company’s inability to meet longer-term growth targets is one reason why I can’t fully buy into this story just yet.

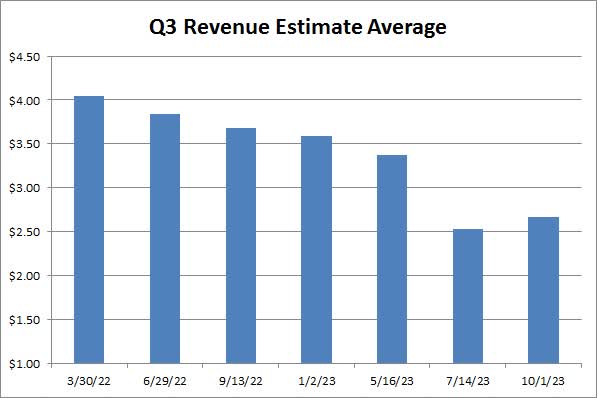

Over the last couple of years, NIO’s struggles to meet its growth targets have resulted in analyst estimates coming down quite significantly. As the chart below shows, the street’s average revenue estimate for Q3 was over $4 billion just 18 months ago. That figure came down to around $2.5 billion this summer until management provided guidance for the quarter, at which point analysts raised their numbers a little bit.

Q3 Analyst Revenue Average (Seeking Alpha)

One thing to remember is that there will be a small headwind to Q3 results when they are translated to US dollars thanks to the strength of the greenback in 2023. Just after this year started, the Dollar / Yuan hit a low of about 6.70, but it has been all uphill ever since. In the company’s Q2 earnings release, all currency translations were made at a ratio of 7.25, but the dollar has strengthened another roughly 0.7% since. We might also see analyst revenue estimates come down a little in the coming weeks since NIO missed the midpoint of its forecast, as analysts were above the company’s midpoint for its Q3 revenue guidance going into Sunday.

As investors look to the current quarter, we’ll probably get October delivery numbers in before the full Q3 report. In the last two years, that report has come in the second week of November, so I’d be looking around the 9th of that month for results to come if that pattern holds. It will be interesting to see if management guides to a new quarterly record for deliveries in Q4, or if there are any other issues like plant upgrades that will result in a sequential decline. Analysts currently expect almost 13% sequential revenue growth in Q4, so there will be some pressure for deliveries to increase, although perhaps some material revenues from the launch of NIO’s smartphone could help a little.

In my previous article, I mentioned how the company’s working capital went negative at the end of Q2. That resulted in another equity offering during July that raised over $700 million. Just recently, NIO completed a convertible note offering, with a chunk of the funds being used to repurchase other debts. I still think another few billion dollars will be needed to execute the growth plan over the next couple of years. If NIO were to raise say $2 billion in early 2024 with this growth track looking good, buying any potential weakness during that capital raise could be a good opportunity for investors.

On the valuation side, NIO currently trades for about 1.20 times next year’s currently expected revenue. That’s slightly below the average of 1.29 times of three other names in the space, Fisker (FSR), Polestar (PSNY), and XPeng (XPEV). NIO right now has the most revenues of the three, but it also has a slightly different business model given its battery swap business as well as its new smartphone segment.

At the moment, I think NIO is fairly valued, which is why I am reiterating a hold rating today. Q3 results took a nice step forward, but the company did miss its guidance midpoint and remains well off its yearly forecast pace. I like the potential growth story here, but NIO needs to prove that it can continue unit sales at these new high levels and do so without recording more major losses and cash burn. For me to upgrade this name to a buy, I’d really like to see another equity raise under the belt, as well as a realistic growth forecast for 2024 that can actually be achieved.

In the end, NIO set a quarterly record for vehicle deliveries in Q3, but the numbers weren’t as strong as they could have been. The company missed the midpoint of its guidance range, and even if Q4 is even stronger, the yearly forecast remains well out of reach, it seems. With the balance sheet still needing a little more help, I can’t jump into this stock yet, so we’ll see over the next few months if the company can do anything to change my mind.

Read the full article here

")

(NASDAQ:PANW)")

")

")

")

2026-04-06")

")

")