")

")

Right now, the consensus outlook for interest rates is that they’re only going to march higher – at least in the short term. With risk-free 5% yields as an appealing alternative, it’s a small wonder that barely-profitable tech stocks have taken losses on the chin over the past month.

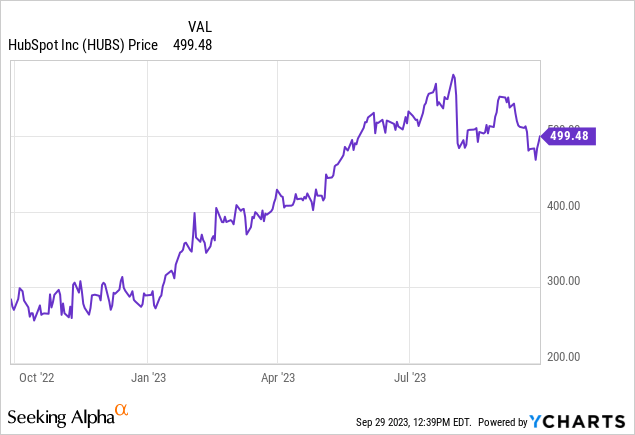

Underneath that broad macro trend, however, there are some major exceptions, and HubSpot (NYSE:HUBS), the inbound sales software platform, has been a big outlier. This Wall Street darling has seen its share price rise by more than 70% in the year to date, and the correction that has happened in tech since July has barely dented its progress.

Another quarter has gone by since I last wrote on HubSpot, and since then its valuation has remained rich while revenue growth has decelerated and interest rates have continued to march higher. Furthermore, the macro outlook continues to be shaky for small and midsized businesses – which is the core market segment that HubSpot targets that differentiates it from larger CRM players like Salesforce.com (CRM). We’ve also seen through the results of other smaller software vendors like Domo (DOMO) that customers are choosing to migrate their software spending away from individualized applications and more toward big-box, portfolio software companies like Salesforce and Microsoft (MSFT) that carry multiple offerings under one platform umbrella.

While we haven’t seen this trend yet affect HubSpot’s results, we are seeing the start of revenue deceleration: which calls into question HubSpot’s massive valuation.

At current share prices just shy of $500, HubSpot trades at a market cap of $24.93 billion. After we net off the $1.67 billion of cash and $455.2 million of convertible debt on HubSpot’s most recent balance sheet, the company’s resulting enterprise value is $23.71 billion.

Meanwhile, for the upcoming fiscal year FY24, Wall Street analysts are expecting HubSpot to generate $2.57 billion in revenue, which would represent 21% y/y growth. In my view, this is quite an aggressive growth target, considering HubSpot’s growth has already decelerated into the mid-20s this year. Nevertheless, even taking consensus estimates at face value, we find that HubSpot trades at a valuation of 9.2x EV/FY24 revenue – quite a steep valuation multiple considering many other ~20% growth software companies have fallen to a ~6-7x revenue multiple (Okta (OKTA) is a good comp here for a company with a similar growth plus margin profile, and it’s trading even lower at just ~5x revenue).

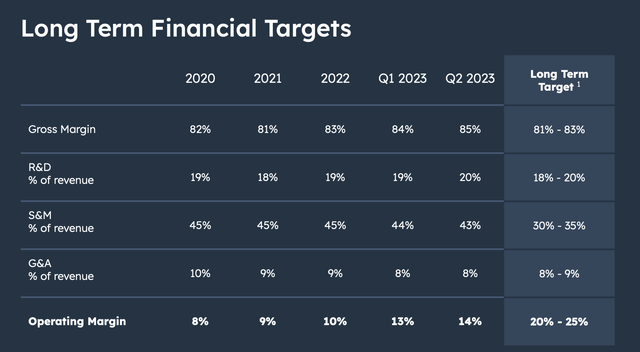

Of course, I understand why investors continue to believe in HubSpot. It is rare among software companies in that it does not deploy a direct sales model, instead relying on inbound marketing (which is the core focus of its software, after all) to drive new customer growth. This sales-light approach has allowed HubSpot to generate immense margins. HubSpot is on the cusp of the vaunted “Rule of 40” metric (the sum of its revenue growth percentage plus pro forma operating margins), which few companies in the software sector are able to achieve.

HubSpot long-term operating model (HubSpot Q2 investor deck)

At the same time, however, I continue to see more risk than opportunity at its current ~$500 price threshold. I see HubSpot dropping off toward the middle of next year; my June 2024 price target on the company is $385, representing 7x FY24 revenue and ~23% downside from current levels.

Sell this stock and invest elsewhere.

Q2 download

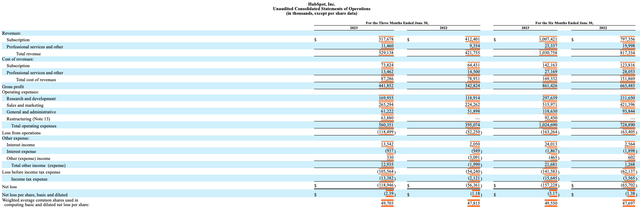

HubSpot had a good showing in its second-quarter earnings release, but in my view not good enough to justify its monster valuation. Take a look at the Q2 earnings summary below:

HubSpot Q2 results (HubSpot Q2 earnings release)

HubSpot’s revenue grew 25% y/y to $529.1 million, ahead of Wall Street’s expectations of $505.5 million (+20% y/y) but decelerating two points versus Q1’s 27% y/y growth rate.

Multi-product adoption continued to be a source of growth for HubSpot: the company noted that now 1 in 3 new deals are buying more than three HubSpot products, which is up by 4% year over year. The company also noted more upmarket traction, especially with Sales Hub – which larger customers are frequently connecting with Service Hub so that sales and support teams can see one unified system of record for open tickets.

Another reason why investors have been bullish on HubSpot is its nascent opportunity in building AI into its product platform. Per CEO Brian Halligan’s remarks on the Q2 earnings call detailing the company’s traction in AI:

We launched ChatSpot earlier this year, and it has quickly grown to 70,000 total users with 20,000 prompts ingested weekly. Our customers tell us that they like our weekly updates. They love how quickly we are innovating with new AI capabilities, and they’re getting value from the breadth of actions ChatSpot is helping them take.

Customers are using ChatSpot to prospects for good fit companies based on location, industry, recent news, and more. They’re creating entire campaigns with SEO research, block title generation, and image generation, all from within ChatSpot. The easy chat interface combined with the power of HubSpot’s platform have our customers eager for what’s next with ChatSpot.

We also launched Content Assistant earlier this year, and since moving it to public beta in June, adoption has grown by 10x, with 26% of our enterprise customers using it today. Customers are describing Content Assistant as a game-changer because they can quickly generate social copy, block content, prospecting e-mails, all based on insights without having to leave HubSpot. Content Assistant embeds Gen AI into our customers’ natural workflow, helping them work faster and smarter, right where they are.

As I look at our AI roadmap, we are ambitiously building AI into the entire CRM platform, so our customers can get even more value from our platform. We want to help scaling companies power their entire customer journey with AI, and we believe we can help them leverage AI better than other platforms for three reasons.”

From a profitability standpoint, HubSpot’s pro forma operating margins rose 700bps y/y to 14%, up from 7% in the year-ago quarter. We note that HubSpot technically fell out of the “Rule of 40” bucket this quarter (its 25% growth plus 14% margin equates to a score of 39, versus 27% growth and 13% margins in Q1).

There’s also potentially worrying news from a billings standpoint, which grew only 22% y/y on a constant currency basis this quarter to $542 million – indicating that further deceleration may be ahead, and in my view is another reason why consensus’ 22% growth expectation for FY24 may be inflated.

Key takeaways

Now is not the time to invest in expensive tech stocks. While HubSpot’s growth at scale and its high-margin operating structure are appealing, they’re already reflected in its rich revenue multiple. Steer clear for now and invest elsewhere.

Read the full article here

")

(NASDAQ:PANW)")

")

")

")

2026-04-06")

")

")