")

")

")

Costco Wholesale (NASDAQ:COST) is a confusing company in the investment world, as investors struggle to find the right balance between its very high quality and its extraordinarily high valuation. While some argue that the nearly 40x P/E leaves no room for upside, others might argue that such quality always comes at a premium.

So, let’s dig deeper into Costco’s business model, and assess whether its current valuation still leaves room for market-beating returns.

5x P/E Or 40x P/E, Which Would You Prefer?

Consider the following two companies. The first trades at a 5x multiple over its last twelve months earnings, and the second trades at a 40x multiple. If that was the only information you had about those two companies, which one would you have picked to add to your portfolio?

Now consider that the first company is some kind of a commodity seller. It had a peak year as its commodity price skyrocketed due to external events that aren’t under its control, and there is huge uncertainty regarding earnings for the next year. Clearly, nobody in the world can come remotely close to predicting where this commodity business will be in ten years. Oh, and it’s highly leveraged because it needed to accelerate capacity quickly to capture the sudden surge in demand.

The second company sells goods that are essential to human lives and for the cheapest price possible. You know that in 10 years, people will still eat, drink, buy electronics and drugs, drive cars, and need furniture. You also know that even if material changes happen to human behavior, this company can always change its product mix accordingly. Furthermore, its infrastructure, geographic presence, and culture, are second to none, and it has a proven track record of being able to expand internationally.

At this point, most investors will have only two answers, either they buy neither of the companies, or they buy the second.

We’re not done yet, though. Consider that the second company grew its EPS at a double-digit rate, in almost every year of its existence. Even if you think it has reached some kind of saturation in its main markets, it has proven that its same-store growth rate is steady in the high-single-digit range. This means that with very high certainty, you might be paying 40x LTM earnings, but less than 30x over its 2025 earnings.

The second company, obviously, is the story of Costco, and while you might think that you should wait for a dip, or you might think that there will be better opportunities to initiate a position, keep in mind that Costco is currently trading at its 5-year average multiple. And, if you bought at almost any point during the last 5 years at that average multiple, you had probably generated very decent returns.

So, let’s dive deeper into Costco, and what makes its business unparalleled to none.

Business Overview

Let’s not overcomplicate this. Costco’s business model is amazingly simple. You pay an annual fee to become a member, and being a member grants you access to shop in Costco’s warehouses, which generally sell goods in bulk, for arguably the cheapest price possible, and with the most welcoming return policy in the world.

The advantages for the consumer are clear, low prices on their essential purchases, and good service. For Costco, some advantages are more clear than others. First, they usually receive the membership fee payments in advance, enabling a favorable cash cycle. Second, those membership fees, by themselves, are essentially carrying near-100% margins. Third, being a member creates loyalty – you’re more likely to shop in a place where you paid for membership. Fourth, the membership system reduces shrinkage (theft), as members don’t want to be banned, and the warehouses are already built to check each entrant.

Membership

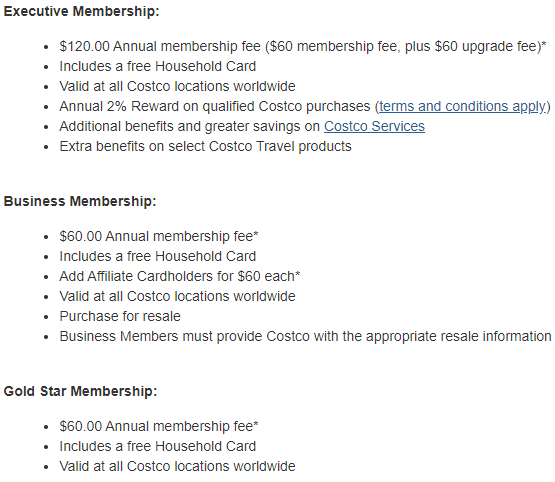

Costco has three membership options, namely, Executive, Business, and Gold Star.

Costco Customer Service, Types of Memberships

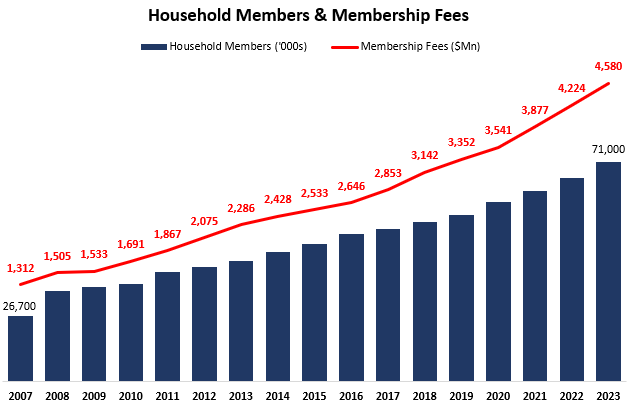

In FY23, Costco generated $4.6 billion in revenues from membership fees. As of the last quarter, Costco had 71 million paying members (households), with 127.9 million cardholders. Executive members represent a little over 45% of members and grew over 3% in the fourth quarter alone. Renewal rates in North America were 92.7% and topped 90.0% worldwide for the second year in a row.

Created by the author using data from Costco Wholesale financial reports (10-K)

One thing of note is that Costco usually raises its membership fees once every five years. However, as a company that sees providing value to customers as its number one competitive advantage, Costco is already “late” by more than six months, as it is trying to postpone the increase to a more convenient macro environment for its customers. More on that in the margin section below.

Warehouses

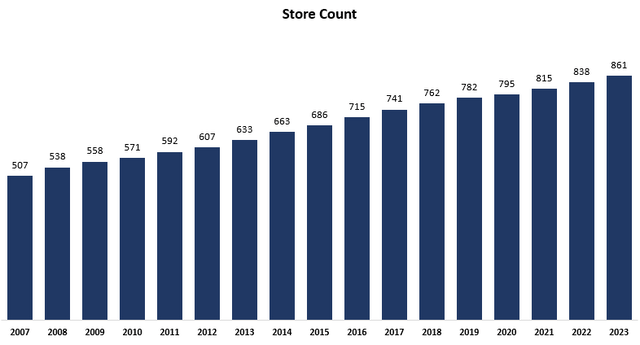

Costco has 862 warehouses worldwide as of October 5th, 2023. 592 locations in 46 U.S. States & Puerto Rico; 107 locations in nine Canadian provinces;29 locations in the United Kingdom; 14 locations in Taiwan; 18 locations in Korea; 33 locations in Japan; 15 locations in Australia; 40 locations in Mexico;4 locations in Spain; 1 location in Iceland; 2 locations in France; 5 locations in China; 1 location in New Zealand; and 1 location in Sweden.

Created by the author using data from Costco Wholesale financial reports (10-K)

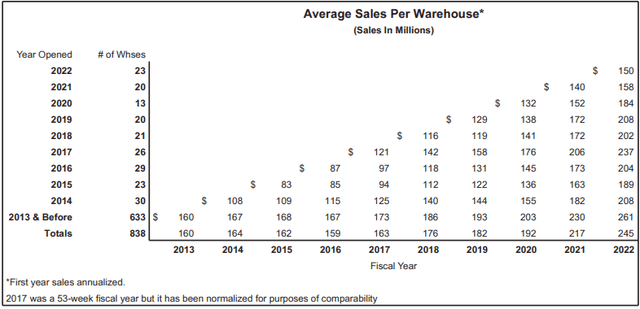

Since 2007, Costco grew its warehouse count by a 3.6% CAGR, but it would be more correct to look at their annual opening pace, rather than growth in terms of percentage. Generally, management is targeting net openings in the 20-30 range, with plans to add 25-30 locations in FY24. Furthermore, despite what some market participants might argue, and actually to the surprise of Costco’s management itself, they believe there’s room to add 150 locations in the U.S. alone, planning to do so over the next 10 years.

Costco 2022 Annual Report

If I had to show one graph to portray Costco, I’d use the above one. We can clearly see two things. One, warehouses grow same-store sales each and every year. Two, as the years go on, new warehouses generate higher revenues from the get-go, reducing the already short ROI period even more.

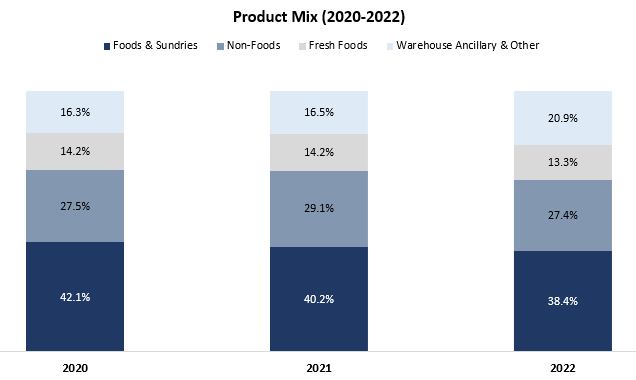

Product Mix

Costco disaggregates its merchandise and services into five categories: Foods and Sundries, Fresh Foods, Non-Foods, Ancillary, and Other.

Foods and Sundries include sundries, dry grocery, candy, cooler, freezer, deli, liquor, and tobacco; Fresh Foods include meat, produce (fruit & veggies), service deli, and bakery; Non-Foods include major appliances, electronics, health and beauty aids, hardware, garden and patio, sporting goods, tires, toys and seasonal, office supplies, automotive care, postage, tickets, apparel, small appliances, furniture, domestics, housewares, special order kiosk, and jewelry; Ancillary include gasoline, pharmacy, optical, food court, hearing aids, and tires; and Other include e-commerce, business centers, travel, Costco Next, and more.

Created and calculated by the author using data from Costco Wholesale financial reports (10-K)

As we can see, Foods & Sundries is the largest category in terms of sales, followed by Non-Foods. Naturally, the Non-Foods category has a more discretionary nature, whereas the other categories are comprised of everyday essentials. According to management, those big-ticket Non-Foods items are pressured by the current macro environment, however, the decline is offset by growth in the other categories.

Margins

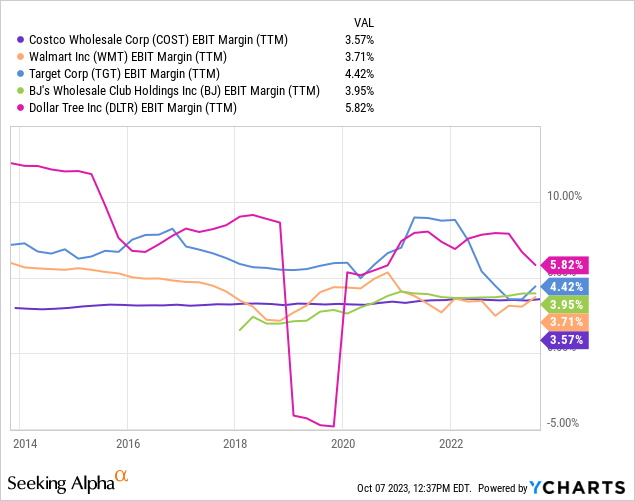

How can you say that somebody doesn’t understand Costco without actually saying it? Well, it’s simple, tell me that he claims Costco’s low margins are a disadvantage.

Above we see a graph portraying the EBIT margins of Costco and four of its major competitors, and I think nothing is more clear than the steadiness of Costco. It’s pretty much a straight line for the past ten years.

Why the competitors’ margins are fluctuating is quite simple, this is a business of buying products from suppliers and reselling them. Such suppliers rely on certain commodities which are always volatile and keep in mind there are matters of logistics, transportation, and a whole lot more.

Why Costco’s margins are so steady, isn’t as obvious. Costco, unlike many other companies, really does put providing value to its customers as its main goal. After all, this is arguably their only true differentiation. As such, Costco passes every price benefit from suppliers directly to its members, with a clear target of 10%-11% gross merchandise profit.

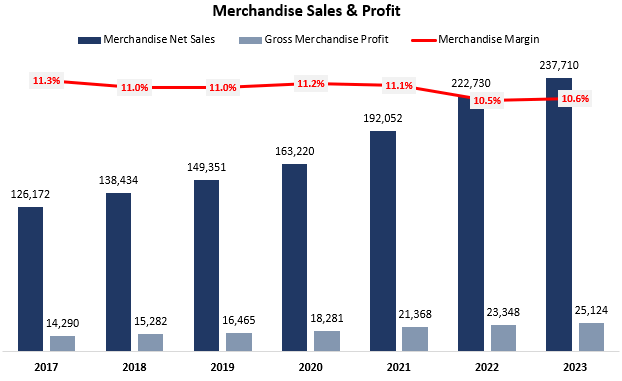

Created and calculated by the author using data from Costco Wholesale financial reports (10-K)

As we can see, gross merchandise margins are quite steady in the 11% range. Overall, it is commonly mistaken by investors that Costco operates its warehouses at a breakeven, and only generates profits from membership fees. In reality, assuming membership fees carry 100% margins, they represent 15.4% of total gross profit and a little over 56.0% of total operating profit.

Costco’s ability to essentially “freeze” its margins is derived from the combination of its business model, and its strong positioning against suppliers, which have a hard time arguing with a company that transfers almost the entirety of the price benefit to its customers. Additionally, Costco’s buyers are highly educated about their relevant suppliers and constantly monitor their relevant markets (for example, they will analyze coffee bean prices before negotiating with coffee suppliers).

Multiple Analysis

With seemingly overvalued companies, I like to look at valuation in a simple multiple-based approach, before heading into discussing my DCF model.

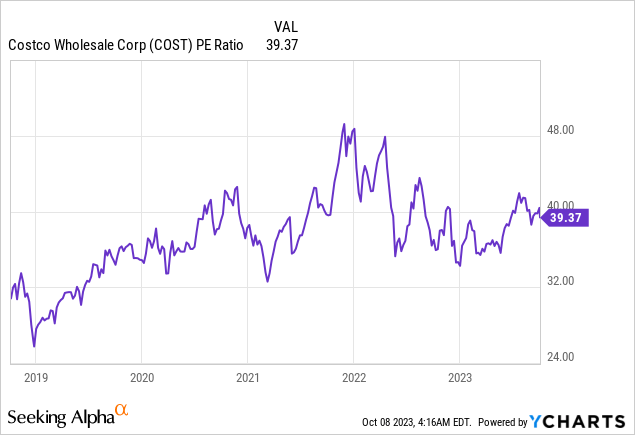

So, let’s begin with discussing Costco’s go-to flaw, which is presumably its high P/E ratio. Costco is currently trading at a 39.2x multiple over FY23 earnings and at a 35.6x multiple over consensus estimates for FY24. Both are pretty much in line with the company’s 5-year average. Taking into account that Costco’s net cash position is at a 5-year high, we can say this is a pretty decent entry point for long-term investors who are bullish on Costco’s future.

By bullish on Costco’s future, I mean investors who estimate Costco will continue to trade at those multiples and will continue to grow its EPS at a double-digit pace. Under these assumptions, combined with steady dividend payments and the occasional special dividend, the path for double-digit annual returns is quite clear.

Personally, for the reasons I discussed in the previous section, you can include me in the above group, and I do plan to initiate a position in the upcoming weeks.

What about the not-so-bullish case? Let’s discuss that. It’s hard to argue with the notion that Costco’s P/E is high. The S&P 500’s average is closer to 20, and the world’s highest-quality companies all trade below the 30x mark. Thus, relying on the fact that Costco continues to trade at these levels, is a shakey leg to lean on.

That being said, Costco’s EPS grew at a CAGR of over 15.1% between FY17 and FY23. It is highly likely that Costco will continue to grow EPS at a double-digit pace for the foreseeable future. As such, I believe the less bullish investors could sit on the fence and wait for another selloff, which will send the valuation closer to the 30x range. As I said, for me, personally, I believe initiating a position now and gradually building it will lead to sufficient returns as well.

Valuation

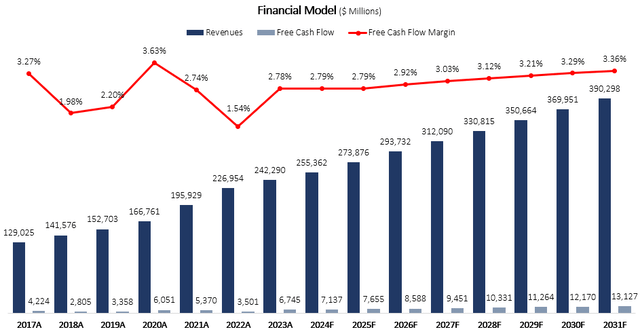

I used a discounted cash flow methodology to evaluate Costco’s fair value. I assume the company will grow revenues at a CAGR of 6.1% between FY23-FY31, based on incremental revenues from 20-30 new units annually, and 6.0% comparable sales growth.

I project free cash flow margins will increase incrementally up to 3.4% in FY31, due to gradual improvements in the company’s cash cycle, constant growth in membership fees, and continued operational leverage resulting from the company’s ability to grow without materially increasing overhead.

Created and calculated by the author based on Costco financial reports and the author’s projections

Taking a WACC of 7.1% and adding Costco’s net cash position, I estimate the company’s fair value at $268B or $604 per share.

Risks

Let’s begin with the elephant in the room, namely, Costco’s valuation. As we discussed above, Costco is certainly not cheap. The company’s fundamentals are quite predictable and usually never surprise (in a good way). They report sales on a monthly basis, and they grow their business slowly and steadily, with no leverage and no rush. Ironically, the combination of these attributes makes it so the stock’s movement is much more sensitive to market sentiment than it is to fundamentals. And we all know we cannot predict market sentiment. If the market decides to sell off Costco, causing a multiple contraction, even a 20% decline won’t necessarily scream a buy, as it will mean Costco is trading at a 28.5x multiple, which is still quite high. However, I believe something extreme needs to happen for the market to turn on Costco, something I don’t see within the realm of reasonable scenarios.

Another risk we should discuss is the uniqueness of Costco’s competitive advantage. The company’s differentiation is not the product it sells. You can get every bit as good as products somewhere else, without paying a membership fee, and usually closer to your home. However, Costco’s advantage comes from price, and customer service (including its return policy). While it seems like a simple business, a change in culture could easily destroy everything that Costco has built over the years. Although I don’t see it anywhere on the horizon, I do think that if Costco’s gross merchandise margin rises above 12%, it would be a major red flag.

Lastly, I think we should mention e-commerce as a risk here. Let’s say it clearly, Costco’s e-commerce business isn’t as good as its warehouses, to say the least. While many thought e-commerce was going to take over the retail landscape during the pandemic, I think we can safely say people like to shop in physical stores, especially at Costco. However, if preference gradually shifts, it is uncertain if Costco will be able to sustain its share in an e-commerce-led world.

Conclusion

Costco is the embodiment of the polarizing argument between value investors and quality-based investors. In my view, “value investors” are those who would buy an inferior company because it’s cheaper, or refrain from buying a high-quality company because its valuation isn’t attractive enough. Quality-based investors would definitely prefer to buy a high-quality company for a cheap price, but they won’t refrain from buying it even for an above-average valuation.

Let me be clear, I believe both strategies are perfectly fine if executed correctly. But I found that for me, personally, a quality-based strategy works better.

While Costco is a polarizing company, even its most stubborn bears will rely almost entirely on its valuation to base their argument, as its business is nearly flawless. With ample room for growth, I rate Costco as a Buy and estimate it will provide market-beating returns in the long term, even and despite its current valuation.

Read the full article here

")

")

2026-04-06")

")

")