")

")

We present our note on Ferrovial (OTC:FERVF), a Spanish multinational infrastructure company with a Buy rating. We are drawn by Ferrovial’s high-quality portfolio of world-class infrastructure assets, positioning in toll roads, and valuation discount. We see 407 ETR traffic improvement back to pre-pandemic rates, and growth in managed lanes as the main catalysts for unlocking value. We will provide a brief overview of the business, lay out our investment case, explain the main drivers and catalysts, and value Ferrovial’s shares using various methodologies.

Introduction to Ferrovial

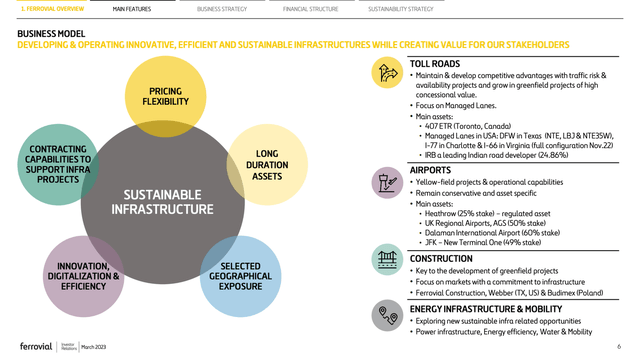

Ferrovial is a leading infrastructure operator and municipal services company. The group operates across four divisions: Toll Roads, Airports, Construction, and Energy Infrastructure & Mobility. The toll roads division is focused on managed lanes, greenfield projects with high concessional value, and traffic risk and availability projects. It contains significant stakes in Canada’s ETR 407 toll road, and managed lanes in the USA including in the Dallas – Fort Worth Area (NTE, LBJ, and NTE35W), Charlotte (I–77), and Virginia (I–66). The airports’ division remains conservative and asset-specific and includes stakes in Heathrow Airport (25%), UK Regional Airports AGS (50% stake), Dalaman International Airport in Southwest Turkey (60%), and JFK – New Terminal 1 in New York (49%). In addition, the firm has a construction division that is key to the development of greenfield projects and allows the company to operate as an integrated infrastructure developer. It includes Ferrovial Construction, Webber, and Budimex (based in Poland). As per analyst estimates referred to in Ferrovial’s investor presentation, 81% of the group’s enterprise value comes from North America, 6% from the UK, 6% from Spain, and 7% from the rest of the world. Ferrovial is dually listed in Spain and the Netherlands and has applied for listing in the US. The company is an IBEX 35 constituent and has a current market capitalization of nearly €22 billion. The founding Del Pino family holds a 35% stake, and 65% of the shares are free-floating.

Ferrovial Equity Story Slides

407 ETR: traffic improving

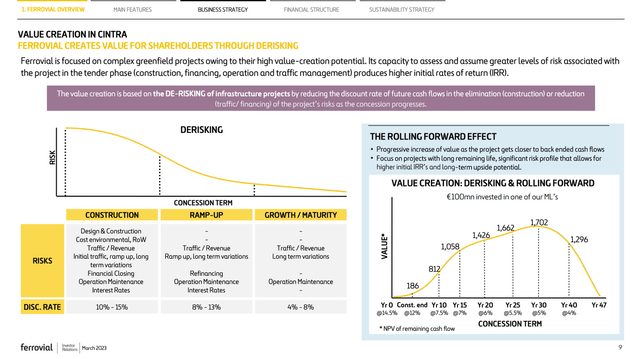

Ferrovial has a high-quality portfolio that consists of long-duration highly cash-generative assets with pricing flexibility. The “crown jewel” of the group: 407 ETR (43.23% Ferrovial stake, accounted using equity method) is a 108 km 400-series highway in Ontario, spanning the entire Greater Toronto Area, an economically vibrant area. The concession has 75 years of maturity and expires in 2098. The highway is fast and reliable and provides a congestion-free alternative to downtown Toronto. Fundamentals are underpinned by robust population and economic growth in the Greater Toronto Area. As per Ferrovial’s investor presentation GTA is expected to grow by more than two million inhabitants in the next two decades, on the back of a strong economy, a growing tech sector, and immigration trends. Moreover, there is significant tariff freedom and flexibility. The flexible tolling regime aims to provide congestion relief in the corridor. 407 ETR can charge different tolls based on segment, time, direction, etc. This has resulted in strong tariff growth of 9% CAGR and EBITDA growth of 11% CAGR in the 2009-2019 decade. 407 ETR has generated a 10x cash return on investment in 20 years.

After a tough period during and after the COVID-19 pandemic, ETR’s traffic is gradually improving to reach levels closer to those of FY2019. Traffic as of the end of Q1 was at 88% of 2019 levels and we expect to converge to up to 95% of 2019 levels by FY2025. This will likely result in lower schedule-22 payments and may proceed with toll rate hikes. The increase in pricing after stagnation despite higher inflation, will drive significant profit growth: EBITDA growing at low double digits per year over the mid-term. Pricing power is underpinned by relatively low cost and significant time savings.

Managed lanes growth

Managed lanes in the US are a key value creation driver for Ferrovial. They provide a choice to users i.e., a solution to congestion in existing roads. The managed lanes concessions have long durations, have pricing flexibility, have little to no collection risks, and benefit from higher than national average population growth, and more favorable macroeconomic conditions. All US managed lanes are now functional and ramping up, with a long growth pathway ahead. In our view, US managed lanes should eventually replicate ETR’s value creation. Moreover, the ramp-up will allow managed lanes to upstream cash to the group, which will in turn be reinvested or returned to shareholders.

Ferrovial Equity Story Slides

Investment case, valuation, and capital returns

We believe Ferrovial’s equity story is remarkably attractive: combining high quality infrastructure assets with higher than GDP earnings growth and long duration, an inflection in cash generation and dividend payment to the HoldCo, and a reasonably cheap valuation.

We value Ferrovial using a free cash flow yield/dividend yield approach. Based on the company’s published internal model and our assumptions we forecast €740 million of dividends from infrastructure assets in the next fiscal year, growing up to nearly €1.1 billion by FY2026. We then assume 0 FCF generation from construction and other activities. (it should be higher, hence this represents some optionality) Historically dividends paid to shareholders have been in line with FCF, and large long-duration quality listed infra companies including Ferrovial itself have been trading at around 3-4% dividend yields. Hence €1.1 billion of dividends implies at least a valuation of €27.5 billion by FY2026 (excluding capital returns in the meantime) implying 28% upside. However, dividends should grow by mid-single to high-single digits well into the future, creating a compounding machine.

We do not have a fixed price target on Ferrovial. We would like to note the stock offers at least a low teens IRR over the mid-term including share price appreciation (at least 28% upside as per our calculation) + dividends.

Risks

Risks include but are not limited to higher than expected real interest rates, lower than expected urban traffic and congestion leading to lower traffic to 407 ETR and managed lanes, delayed pipeline executions, higher competition, structurally lower mobility, higher than expected penalty payments, adverse FX changes, adverse regulatory and legal changes, misallocation of capital including value destructive M&A, etc.

Conclusion

Given the attractive fundamentals combined with compelling fundamentals and catalysts, we recommend buying Ferrovial shares.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

(NASDAQ:PANW)")

")

")

")

2026-04-06")

")

")