")

")

")

Why ET is a stronger buy despite price rallies?

I last wrote on Energy Transfer (NYSE:ET) a bit more than three months ago (see the chart below). The article argued for a buy thesis on the stock. The thesis was built mainly on three pillars at that time. First, I argued that the softened commodity pricing environment up to that point was temporary. Second, and in addition to a potential recovery of commodity price, I also argued that its strong volume and add-on acquisitions can further help the topline grow. Finally, I argued that the stock offered a sizable valuation discount at that time. To wit, its market P/E was about 14% below the Graham P/E.

Fast-forward to now, the stock has indeed delivered strong returns against an overall market decline. To wit, the stock has enjoyed a 7.6% price rally and delivered a total return of more than 10%. While in contrast, the S&P 500 lost about 2% in the same period.

Despite the price rally, I see the stock as an even stronger buy at this point, and consequently, this article will upgrade my rating to Strong Buy. In the remainder of this article, I will elaborate on two of my key considerations for my upgraded rating. First, I will argue that a few new catalysts have happened since then, and they can provide ET with a better growth potential. Second, because of such a better growth potential, the stock valuation has actually become even more discounted from the Graham P/E.

The new catalysts

Oil prices have recovered strongly since my last article. As seen from the chart below, Brent futures were in the $75 range at that time. It has since then reached a peak of almost $100 and currently hovers around $87. Now, I see a couple of catalysts to keep oil prices (or energy/commodity prices in general) elevated and provide a tailwind for ET in the near future.

Seeking Alpha

The most important catalyst in my view, sadly, is the ongoing conflict between Israel and Hamas. In general, geopolitical risks tend to increase demand for oil and commodities for several reasons. Geopolitical conflicts tend to disrupt supply, transportation, and global trading. At the same time, both the general public and investors may seek to store more commodities as a hedge against the ongoing geopolitical conflicts.

Specific to the Israel-Hamas conflict, I see more immediate impacts on oil and energy prices. The conflict could have nonlinear ramifications on other countries in the Middle Eastern region, many of which are important oil production/export countries. Iran is the first specific example that came to my mind. Iran is a significant oil production country and also a known supporter of Hamas. As such, it’s a possible scenario, in my view, we could see a tightening of restrictions on Iranian oil exports.

Admittedly, these catalysts are relevant to the general energy sector and won’t only serve as a tailwind for ET. However, I will argue that thanks to a few differentiating factors, ET is better positioned to navigate the ramifications of such geopolitical events than the sector average. The top differentiators are its scale and integrated operations. ET is one of the largest and most diversified midstream energy companies in North America. Its assets are highly integrated, which allows it to achieve significant operational efficiencies. For example, its pipeline network connects production areas to processing facilities and storage terminals, which allows the company to move products quickly and efficiently to market.

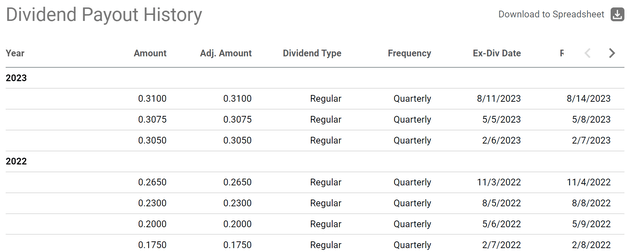

This unique strength has provided ET with the resilience to deliver strong results amid market turmoil. The following chart shows its recent dividend payouts as a reflection of such resilience. As seen, the dividend amount has recovered very quickly since the COVID-19 pandemic. It increased rapidly from $0.175 per share in the first quarter of 2022 to $0.31 per share at this point. This represents an increase of approximately 77%, and its current payout already is higher than its pre-pandemic level of $0.305 per share.

The stock is currently yielding 9.06% on an FWD basis. Such a high yield, when combined with its resilience and discounted valuation (argued next), makes it a strong income generator in uncertain times like this.

Seeking Alpha

Market price vs. Graham P/E

For the valuation of a “traditional” business like ET, I will follow the Graham approach as detailed in his book (Intelligent Investor). In particular, I will start with the so-called Graham P/E. As detailed in my earlier article:

Graham recommended the P/E for a defensive stock should be around 8.5 plus twice the expected annual growth rate, which I call the Graham P/E. Hence, in his mind, a business that completely stagnates should be worth about 8.5x P/E.

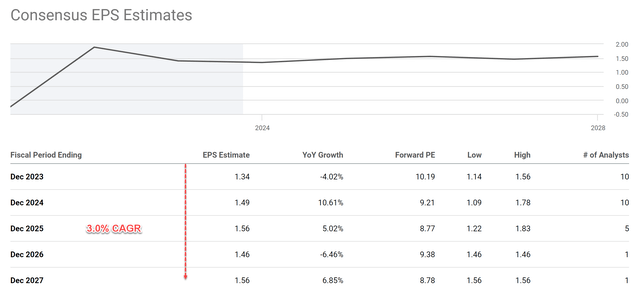

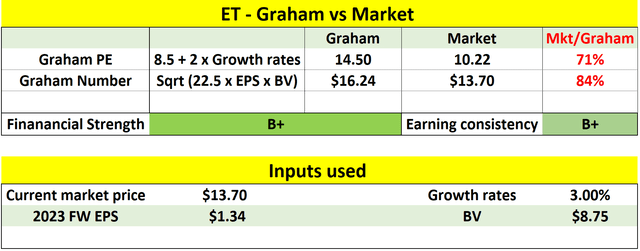

In ET’s case, consensus estimates project an EPS growth rate of ~1% CAGR at the time of my original article. The above projection was too pessimistic in my view. But even with a 1% growth rate, its Graham P/E would be 10.5x. At that time, the stock was trading around a P/E of 9.06x, about 14% below the Graham P/E. Now, due to the recovery of commodities prices and the other catalysts mentioned above, consensus estimates have upped the growth projection in the next few years to 3.0% as seen in the chart below.

With this new growth rate, the discount has become larger despite the price rallies since as shown in my next table. As seen, its market P/E is about 10.22x currently, about 29% lower than the Graham P/E.

Seeking Alpha Author based on Seeking Alpha data

Risks and final thoughts

There are a few other risks both in the upward and downward directions that are worth mentioning. In the upward direction, ET’s assets are primarily located in the United States, which makes ET less exposed to the risks associated with geopolitical conflicts in other parts of the world than the sector average. Furthermore, its revenue model is primarily fee based. It charges a fee for transporting, storing, and processing energy products for its customers. As such, its revenue model is less exposed to geopolitical events should they take an unexpected turn.

In the downside direction, the Graham Number shows a smaller discount, as you can see from my analyses table above. The Graham P/E only takes into consideration the EPS, while the Graham number considers both the earnings and the book value. As such, the fact that the Graham number shows a smaller discount implies that the market is giving its assets a more favorable price than its earnings. But still, the Graham number also shows a sizable valuation discount of 16%.

To conclude, despite the price rally since my last writing, I view ET as an even stronger buy under current conditions. The main factors involved in this upgrading are twofold. First, I see new catalysts that can support a better growth potential (and so do consensus estimates). Second, because of the better growth potential, I see its valuation as more discounted now compared to the time of my last writing.

Read the full article here

")

")

2026-04-06")

")

")