")

")

")

Just six months, I warned on Calibre Mining (OTCQX:CXBMF), noting that while the stock remained one of the more attractively valued names sector-wide, it was pushing into nosebleed territory from a technical standpoint and that rallies to US$1.20 would provide an opportunity to book some profits. And while the stock initially pushed higher, it’s since suffered a ~28% drawdown from these levels void of any negative fundamental developments, instead dragged down by the weight of overall sector weakness. Fortunately, this correction has improved the stock’s reward/risk setup and the fundamental picture remains stronger than ever. This is because Calibre will end the year with well over $100 million in cash and another record year for production, reserves, and resources and, most importantly, per share growth in these key metrics. Let’s take a closer look:

Calibre Mining Operations – Company Website

All figures are in United States Dollars unless otherwise noted.

Q3 Production

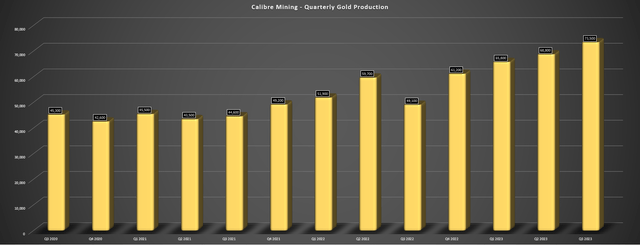

Calibre Mining released its Q3 results this week and reported another blowout quarter, with ~73,500 gold ounces of gold produced – a 4th consecutive record quarter for the company. The impressive results translated to 50% production growth year-over-year, an industry-leading figure, and they were driven by its Nicaraguan asset base. In fact, Nicaraguan production of ~63,800 ounces represented a significant increase from the previous record of ~50,700 ounces, helped by a full quarter of contribution from its new high-grade Eastern Borosi spoke (part of its Hub & Spoke model). However, while Nicaraguan production has grown to a ~240,000 ounce annualized run rate, it’s important to note that the company has considerable gas left in the tank for this jurisdiction, with over 800,000 tonnes of excess milling capacity, multiple new discoveries with maiden resources/reserves, and a land package that remains ripe for future discoveries.

Calibre – Quarterly Gold Production

Moving over to the company’s Nevada operations, its Pan Mine produced ~9,700 ounces in the period, a dip from the 10,000+ ounces produced in the previous five quarters, but the mine remains on track to meet its FY2023 guidance midpoint of 42,500 ounces, with production sitting at ~76.7% of this figure with one quarter to go. And on a consolidated basis, the company noted that it expects to deliver into the high end of its 250,000 – 275,000 ounce guidance range, with this set to mark yet another year that the company will trounce its guidance mid-point, with company-wide production currently sitting at ~79% of its mid-point (~262,000 ounces). Overall, this is very positive, given that there are few miners that have been able to consistently over-deliver on promises like Calibre, providing confidence in this team to deliver on what look to be their larger plans to become a 350,000 ounce per annum producer.

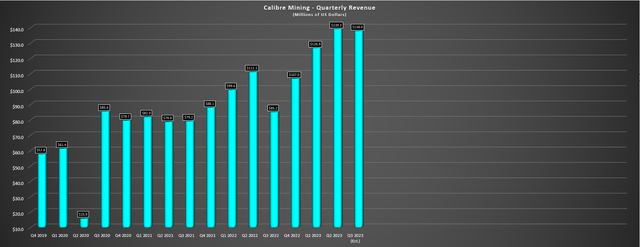

Calibre – Quarterly Revenue

Finally, digging into sales, Calibre should have another record or near-record quarter from a revenue standpoint, assuming the company sells at least 72,000 ounces at $1,915/oz or higher, translating to revenue of ~$138 million. This strong financial performance combined with a better gold price this year should allow Calibre to generate at least $175 million in operating cash flow, which would represent ~65% growth on a two-year basis, with a path to $190 million in operating cash flow next year if the gold price cooperates. And from a free cash flow standpoint, this should translate to upwards of $85+ million in free cash flow next year. So, with one of the strongest balance sheets among junior and mid-tier producers (~$80 million in net cash), and a low-cap organic growth opportunity, Calibre remains of the better growth stories in the sector, with the ability to forego new plant construction to increase output being a key differentiator.

Unlike other producers, that will see significant capex bills to increase production and could be impeded by permitting timelines, Calibre’s speedy permitting approvals and ability to haul ore to a central facility with excess capacity means it needs to focus solely on exploration/underground development vs. a full build at a greenfield or brownfields site (plant, mine, tailings, associated infrastructure) which can be much costlier.

Recent Developments

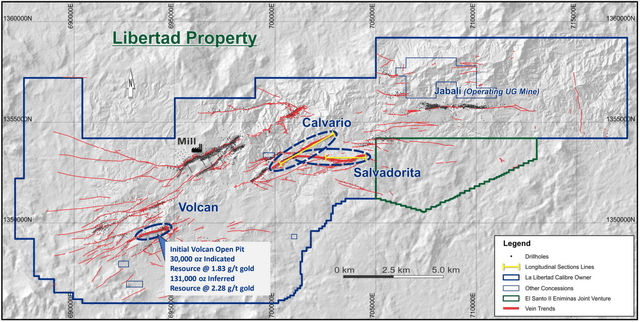

While Calibre continues to fire on all cylinders from a production standpoint, the company is arguably doing an even better job with the drill bit, making a potential game-changing discovery at Panton North (El Limon Property) with further upside along the VTEM corridor, and recently releasing a maiden resource for the Volcan Open Pit which lies just 5 kilometers from its Libertad Plant at its Libertad Property. Digging into Volcan, the company has announced a combined resource of ~161,000 ounces of gold (~508,000 tonnes of indicated material at 1.83 grams per tonne of gold and ~1.79 million tonnes inferred at 2.28 grams per tonne of gold) which could potentially be moved into production by 2025 and take advantage of the excess capacity at the nearby mill.

Libertad & Maiden Volcan OP Resource – Company Website

When discussing the resource, Calibre’s Senior Vice President of Growth stated:

“I am encouraged by additional geoscience indicators that appear similar to Volcan, situated across the Libertad property and we look forward to results from these exciting new targets that surround our under-utilized Libertad mill”.

– Tom Gallo, Senior VP Growth, Calibre Mining

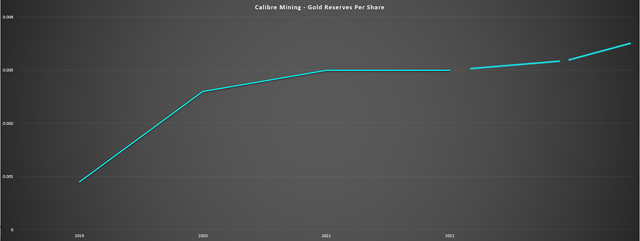

As shown in the above map, two other opportunities at Libertad are Calvario and Salvadorita, where the company which contains high-grade surface samples of up to 21.2 grams per tonne of gold, with these opportunities adding to a growing resource base in Nicaragua that came in at ~2.6 million ounces between Limon, Libertad, Pavon and Eastern Borosi across all categories and has since grown to just shy of ~2.8 million ounces with the release of a maiden resource at Volcan OP. And given that the company has been able to self-fund its growth and will continue to do so with its strong balance sheet, this should lead to continued growth in reserves per share, a metric where Calibre continues to lead its peers given its low discovery cost per ounce and low hurdle to adding reserves (considerable sunk costs at Libertad).

Calibre Mining – Reserve Per Share Growth & Future Growth – Company Filings, Author’s Chart

So, what’s the opportunity here?

While the company is going to take a disciplined approach to putting Panteon North/Northwest into production, which will provide another high-grade feed source on top of Eastern Borosi, there looks to be the potential to grow its Nicaraguan production profile alone to 310,000+ ounces by 2027. And assuming the company can maintain a 50,000+ ounce production profile in Nevada, this would translate to at least a 360,000 ounce production profile, pointing to 30% production growth vs. the top end of its FY2022 guidance in the next four years. Hence, I would expect Calibre to continue to be one of the better per share growers in its peer group, with consistent growth in resources, reserves, production and cash flow per share, and possibly a dividend eventually for patient shareholders. Let’s look at the valuation:

Valuation

Based on ~501 million fully diluted shares and a share price of US$1.02, Calibre Mining trades at a market cap of ~$510 million and an enterprise value of ~$440 million, giving it one of the lowest capitalizations among the 200,000 to 300,000 ounce producer space. This leaves the stock trading at barely 4x FY2024 EV/FCF estimates, making it one of the cheapest producers sector-wide. Hence, for investors looking for value in this market and comfy with owning a name with the bulk of its production coming from a less attractively ranked jurisdiction, Calibre is certainly one of the better buy-the-dip candidates out there. That said, I am looking for a minimum 40% discount to fair value when starting new positions in small-cap names with the bulk of their NAV tied to higher-risk jurisdictions, so while I would become interested in CXBMF on further weakness, I see an ideal buy zone of US$0.89 vs. its updated fair value estimate of US$1.48 (18-month target price).

Summary

Calibre Mining continues to be one of the best run junior producers in the gold sector, with impressive exploration success, consistent production records and a balance sheet and hungry mill that can support production and free cash flow growth with any share dilution. This is a key differentiator given that most junior producers (and even some mid-tiers) are diluting each year, meaning that while cash flow, resources and production are growing, there’s little benefit for shareholders as per share metrics are stagnant. Plus, as noted earlier, I see a stretch target of 370,000 to 400,000 ounces by 2028 for Calibre if it can execute successfully, making it one of the better growth stories in the sector today. In summary, I see Calibre as one of the top-10 small-cap producers sector-wide and I would view any pullbacks below US$0.88 as buying opportunities.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

2026-04-06")

")

")