")

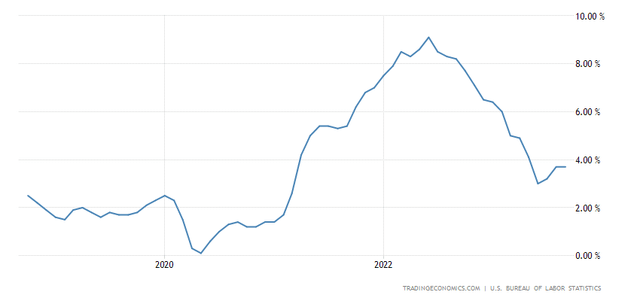

Last summer, I asserted that the rate of inflation would fall as fast as it rose, based on the assumption that its increase was fueled by one-time factors related to the pandemic, post-pandemic stimulus, and the war in Ukraine. That forecast was met with great rebuke, as it was so far from the consensus view that it wasn’t even on the map at the time. It took 16 months for the annualized rate to rise from 2% in February 2021 to 9.1% in June 2022. It took 12 months to fall back to 3% in June of 2023 before rebounding to 3.7% over the past three months on more difficult year-over-year comparisons for energy prices. Still, that is not far from the mark, which I think gives me some credibility in stating that we will see a 2% handle on the rate before the year end.

Finviz

The Consumer Price Index (CPI) report for September unequivocally tells us that the disinflationary trend is intact, and that the Fed’s 2% target rate is on the horizon, but you wouldn’t know it from yesterday’s market response or the commentary that came with it. The 0.4% monthly increase in the headline number was a tick higher than the 0.3% expected, resulting in the same 3.7% annualized rate that we saw the month before. The inflation hawks came out of the woodwork, warning that the threat of an inflation resurgence can’t be ignored. Traders sold bonds, yields rose, the dollar strengthened, and stock prices fell sharply after four days of gains. This was clearly a knee-jerk reaction to one-tenth of a tick in the wrong direction, but a deeper look reveals that we are still right on track for 2%.

TradingEconomics

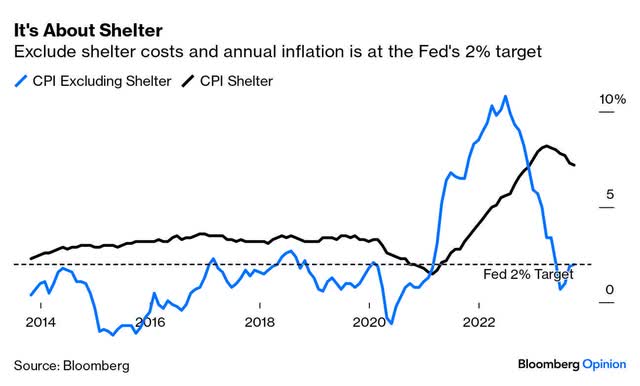

It all boils down to shelter costs, which I have been pounding the table on for months. When we exclude the cost of shelter from the index, the rate of inflation has already fallen to the Fed’s target of 2%.

Bloomberg

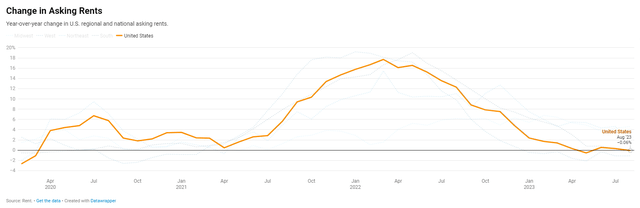

The increase in shelter costs is still running at an annualized 7%, because the measurement includes price increases for all leases in force over the past 12 months. Therefore, this category operates within the CPI with a significant lag. The increase in prices for new leases on a nationwide basis is negligible today, as seen in the chart below, but it will take several more months to work these new monthly numbers into the 12-month calculation. Once that happens, all else equal, the Fed will have reached its 2% inflation target. I might be concerned about a rebound in rent prices, but with more than 460,000 new units on track to be completed this year alone, and the number of new units under construction at a 50-year high, the increase in supply should keep prices in check.

Rent.com

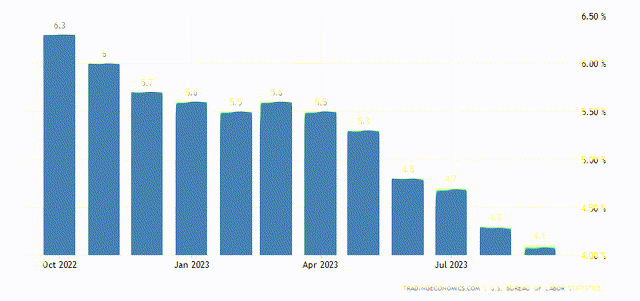

The core rate in September was in line at 0.3% for the month. The core, which excludes food and energy, is favored by the Fed because it is a better measure of underlying inflation than the overall CPI. The core rate declined from an annualized 4.3% to 4.1%, as expected. Again, the most heavily weighted category in this index is shelter, which should bring this number down to target in the coming months.

TradingEconomics

Inflation is the most lagging of all economic indicators, while changes in the Fed’s interest-rate policy can take as long as a year to have an impact on economic activity. This is why it makes absolutely no sense to suggest that another interest rate increase is required based on an inflation report that looks backwards over the past 12 months. Yet market pundits and Fed officials do it every month. The current Fed funds rate at a range of 5.25-5.5% is overly sufficient to achieve stable prices, which is why I think the rate-hike cycle has ended, despite what some Fed officials say. Furthermore, I think the rate cuts will come sooner than the consensus expects as we achieve stable prices well in advance of the Fed’s more recent economic projections.

Read the full article here

")

2026-04-06")

")

")