")

")

Zillow’s (NASDAQ:Z) business and share price have held up surprisingly well in 2023, in the face of rising mortgage rates and an anemic real estate market. While Zillow has a large opportunity and appears better positioned after abandoning its iBuying efforts, the recent move higher in long-term bond yields is beginning to take a toll. Housing market dysfunction is increasing, and investors are unlikely to look through weakness indefinitely.

Market

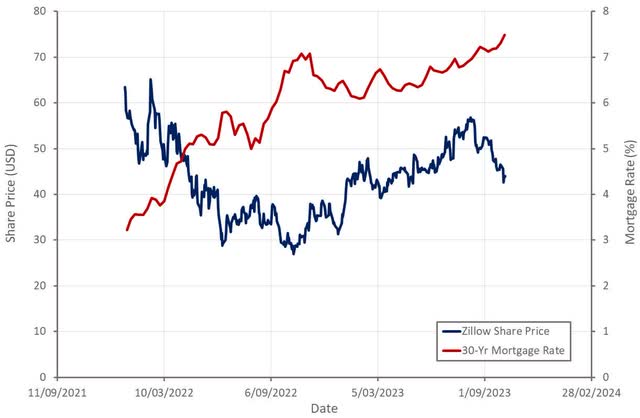

Continued economic strength, along with builder rate buy downs, have helped Zillow’s stock move higher in 2023 despite rising mortgage rates. The recent move higher in rates appears to have caused a shift in investor sentiment though, possibly due to a recognition that the current situation will not be resolved without significant pain.

Figure 1: Mortgage Rates and Zillow Share Price (source: Created by author using data from The Federal Reserve and Yahoo Finance)

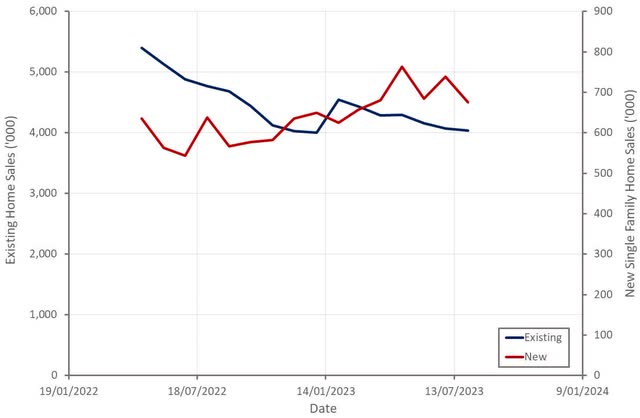

While home sales in the US remain depressed, Zillow’s business is being somewhat aided by relative strength in new home sales. Builder incentives are allowing this market to thrive, even as mortgage rates move higher. This situation may not persist indefinitely though, particularly if the broader economy weakens and begins to undermine buyer sentiment.

Ultimately, either mortgage rates or home prices will need to move significantly lower in order for transaction volumes to recover to more normal levels. The current stalemate may need to be resolved by a recession though, which would not be without short-term pain for Zillow.

Figure 2: Existing and New Home Sales in the US (source: Created by author using data from The Federal Reserve)

Zillow

More than 80% of Zillow’s traffic is direct, and it is this traffic that provides Zillow with both a large opportunity and a competitive advantage. Previous efforts to monetize this traffic through iBuying were a failure, but Zillow’s current strategy stays closer to the company’s core competencies.

While market conditions continue to be difficult, Zillow’s business is significantly outperforming the broader market. Zillow’s rental business is benefitting from the record level of new supply and rapidly rising vacancy rates, which are creating demand for rental advertising. In addition to Zillow’s traditional core business, Zillow is also focused on driving growth through:

- Touring

- Financing

- Seller solutions

Zillow hopes that success in these areas will help it to grow its share of customer transactions from 3% to 6% by the end of 2025. It should be noted that these businesses are not particularly material to Zillow’s business at this point in time though.

Zillow believes that approximately 25% of all US homebuyers sought a Premier Agent partner in the previous year, but only an estimated 3% of home buyers and sellers ultimately transacted with Zillow. This demonstrates that Zillow still has a large opportunity ahead of it, even if this currently being hidden by muted home sales figures.

Approximately 1 in 3 Premier Agent partners in Zillow’s enhanced markets are connecting customers to Zillow Home Loans, up from roughly 1 in 5 in Q4 2022. Purchase loan origination volume increased 73% YoY in the second quarter and 30% sequentially. The financing business is likely to continue to struggle while mortgage rates remain at current levels though.

Zillow has now rolled out real-time touring in all 6 of its enhanced markets and has now begun launching outside of its enhanced markets.

In support of its Seller solutions, Zillow recently acquired ARIA, a software provider to real estate photographers across the US. ARIA’s platform capabilities and network of third-party real estate photographers will help enable the company to scale ShowingTime’s listing showcase product.

Zillow also recently announced the sunsetting of Zillow Closing Services. Integrating the real estate transaction to make buying and selling simpler remains a core part of Zillow’s strategy but the company felt that the Zillow Closing Services product was not suitable. Zillow is exploring alternative title and escrow solutions.

Financial Analysis

Zillow’s revenue was 506 million USD in the second quarter, beating the high end of the company’s outlook by 27 million USD. Outperformance has been driven by Zillow’s execution and market conditions not deteriorating as much as expected. Residential revenue was 380 million USD, down 3% YoY compared to an industry decline of 22%. Rentals revenue increased 28% YoY, with Rentals traffic growing 15% YoY to 31 million average monthly rental unique visitors. Mortgages revenue was 24 million USD, with purchased loan origination volumes growing 30% sequentially from Q1 and 73% YoY.

Third quarter revenue is expected to be between 458 million USD and 486 million USD, a 2% YoY decline at the midpoint. Residential revenue is expected to be down 6% YoY compared to an industry transaction dollar decline of 15-20%.

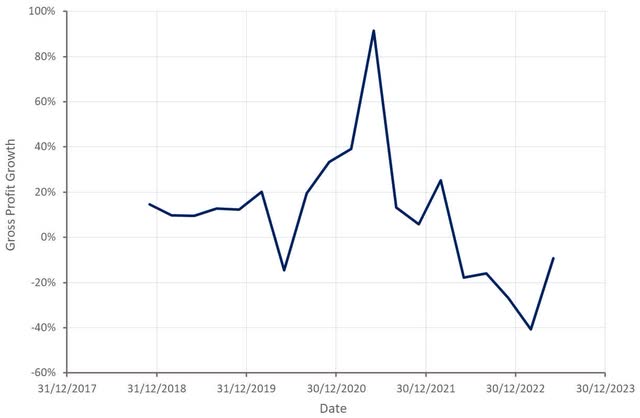

Figure 3: Zillow Gross Profit Growth (source: Created by author using data from Zillow)

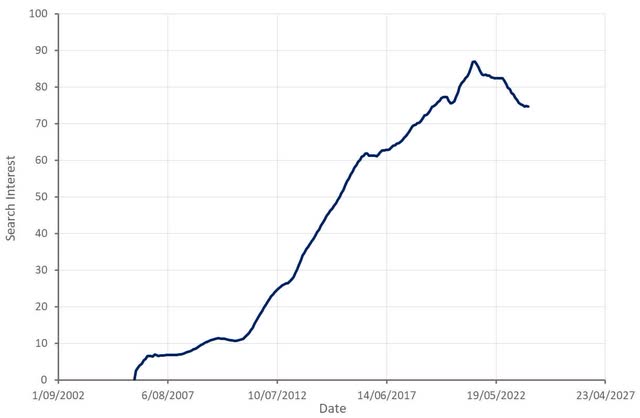

Search data seems to indicate that demand for Zillow’s services has levelled off over the past 5 months, although is down significantly from the peaks registered in 2021. While the worst of the revenue declines may now be behind Zillow, it is difficult to see the company returning to healthy growth until mortgage rates decline.

Figure 4: Zillow Search Interest (source: Created by author using data from Google Trends)

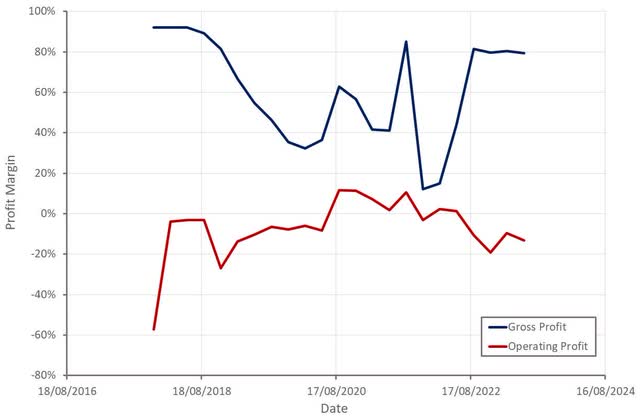

Zillow’s gross profit margins have fully recovered from iBuying business exit and have been stable at around 80% in recent quarters. Operating profit margins have continued to decline on the back of lower revenues though. This situation should naturally resolve itself when market conditions strengthen but will also be aided by Zillow’s efforts to drive operational efficiency. For example, loan officer productivity increased by 50% between Q4 2022 and Q2 2023 based on the number of locked loans. Zillow’s management team have suggested that the company’s fixed cost run rate is approximately 1.1 billion USD annually, and that its variable cost run rate is approximately 400 million USD annually.

Share-based compensation amounted to 130 million USD in the second quarter, with the sequential increase driven by departing personnel and the impact of Zillow’s March 2023 annual employee grants. It should be noted that SBC is running at around 25% of revenue, which is quite high and will make achieving high margins difficult in the near term.

Figure 5: Zillow Profit Margins (source: Created by author using data from Zillow)

Valuation

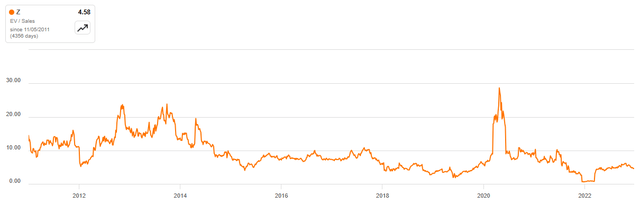

Zillow has always been a business with a large amount of potential, but it has never really managed to create significant value for shareholders. This could change if the company can execute its current strategy, but the current tenuous state of the housing market is a risk. While Zillow’s valuation isn’t particularly high, I do not believe it is low enough to compensate for potential near-term downside risk.

Figure 6: Zillow EV/S Multiple (source: Seeking Alpha)

Read the full article here

")

2026-04-06")

")

")