")

")

")

Some Introductory Thoughts Before A Brief Financial Analysis

After years of waiting to buy CrowdStrike (NASDAQ:CRWD), I struck, so to speak, in late November of 2022 at $112/share, and I recently shared an update on the business here in the link below:

- CrowdStrike Holdings Stock: Right In The Strike Zone (CRWD).

For those that were likewise buying in late 2022 and early 2023, I think we will generate fairly easy 20%+ annualized returns from that level over the next decade.

And I think we’ll do quite well from $149/share as well. After some introductory thoughts and a brief financial analysis, I will consider the valuation of CrowdStrike at ~$188/share with you.

Similar to the trading dynamics of so many of the businesses that I own, CrowdStrike should have never traded to nearly $300/share, and it should have never traded to nearly $90/share.

Throughout the entire process of CrowdStrike’s share price overshooting to the upside and overshooting to the downside, the reality of CrowdStrike’s intrinsic value (the net present value of its future cash flows) has been somewhere in the middle.

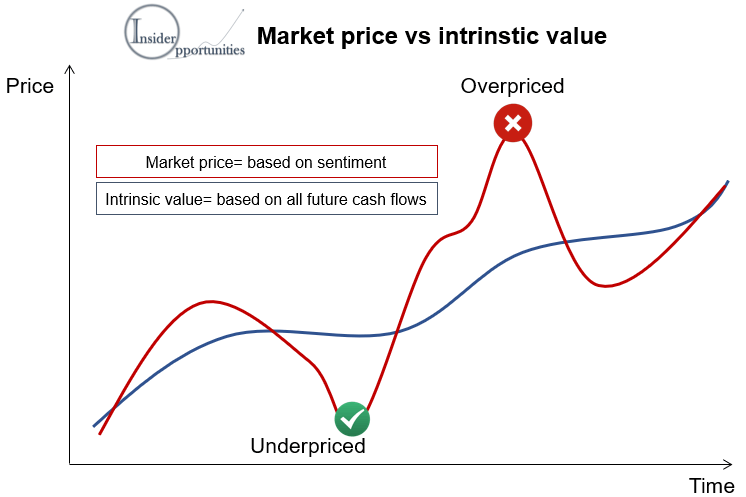

I often share the following chart with you, but it certainly bears repeating, as virtually all of the companies I share with you, from Amazon (AMZN) and Chipotle (CMG) to Affirm (AFRM) and Marqeta (MQ) to S1 (S) and Monday (MNDY), will find themselves with a chart that looks similar to the chart below as time passes.

Insider Opportunities On Seeking Alpha

- Note: Of course, the above chart and the following charts do not represent exhibitions of an exact science. The charts do represent a loose approximation of businesses’ shares prices compared against the growth of free cash flow per share for these businesses. Free cash flow per share is the essential undergirding variable of all equity value (the equivalent for bonds would be the bond’s coupon or the interest that’s paid out by the bond, also known as yield).

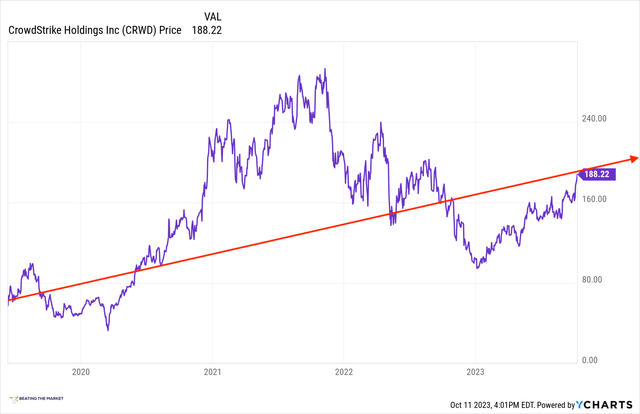

CrowdStrike’s Share Price Vs Its Intrinsic Value

YCharts

And a couple more for context:

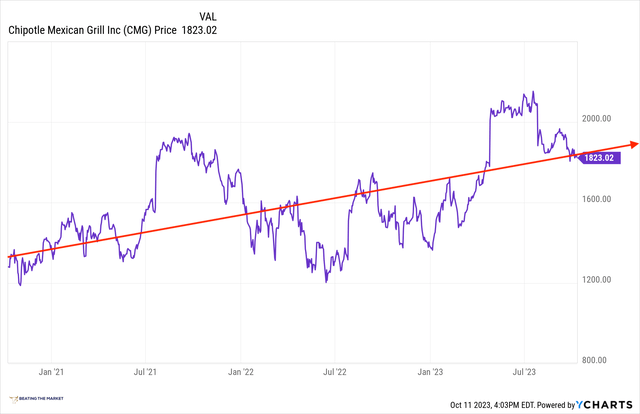

Chipotle’s Share Price Vs Its Intrinsic Value

YCharts

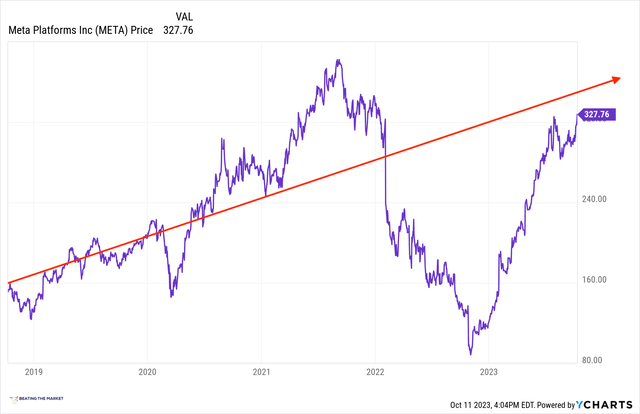

Meta’s Share Price Vs Its Intrinsic Value

Meta

(Yes, I think Meta remains very undervalued).

Again, the above exhibitions of intrinsic value against share price dynamics are not exact in any remote sense. They are however exhibitions of timeless truth related to the nature of how equities’ prices fluctuate around their intrinsic values.

Shifting our focus to CrowdStrike, as I’ve been noting quite often lately, with the help of our beloved community member Stephan1989, CrowdStrike has been trading at what I could consider its fair value, where risk (15-25% annualized returns) = return (15-25% annualized returns).

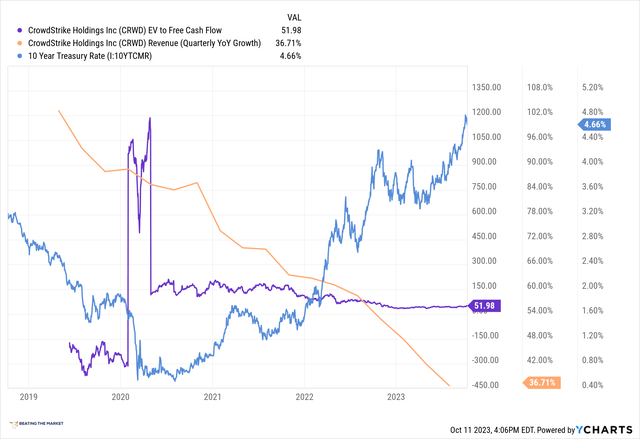

A nuanced view of CrowdStrike’s valuation can be seen below:

CrowdStrike’s EV/FCF & Quarterly Revenue Growth; The 10-Year Treasury Bond Yield

YCharts

Notably, CrowdStrike’s valuation has not fallen in a vacuum.

As I’ve discussed with you in the past, interest rates are to equity valuations as gravity is to matter.

The higher the interest rates, the stronger the downward pull on valuations.

The stronger the gravity, the stronger the downward pull on matter.

And, as the chart depicts, interest rates in the U.S. economy have risen, as we all know quite well by now, at the fastest rate in American history, which has, in part, afforded us the ability to accumulate CrowdStrike at much more sober and attractive valuation levels over the last 12 months.

Additionally, higher interest rates also pull down on economic growth, which, by extension pulls down on CrowdStrike’s growth, and the above chart depicts as much.

Slower sales and profit growth also act as anchors on valuations. That is, as growth slows, all else being equal, a company’s valuation, such as EV/FCF or price to earnings ratio, will compress, as we’ve witnessed for CrowdStrike and virtually all of the companies within our coverage universe.

To this end, the valuation dynamics depicted above are not idiosyncratic to CrowdStrike. I have spent the better part of the last two months detailing repetitively the idea that the macroeconomic environment has meaningfully deteriorated on the heels of the fastest interest rate hiking cycle in American history, and this has caused industries like software and digital ads to experience collapsing growth rates.

Of course, as I’ve also often noted, this has created the exceptional opportunity we’ve been afforded over the last year or so, on which we’ve capitalized.

Were it not for the deterioration of the economy broadly, we’d not have had the opportunity to buy many of our favorite businesses of the last half decade or so at the attractive valuation levels.

To close this brief introductory section, a confluence of factors have conspired to provide us the opportunity to sustainably accumulate CrowdStrike throughout late 2022 and the entirety of 2023 at attractive valuations, and, despite the rather ebullient broad market sentiment in the last 6 months, I do not believe CrowdStrike is unattractively priced at $190/share, where it currently trades, especially in light of CrowdStrike’s recent guidance update, in which it revealed that it believes it will achieve 35-38% free cash flow margins, up from its current ~30% free cash flow margins.

I believe the vast majority of my coverage universe remains quite attractively priced, which is fairly ironic, because my coverage universe mostly consists of younger (10-30 years old) businesses on which the consensus of market participants agreed were incredible businesses for the better part of the last decade, but have since abandoned that conviction for one reason or another.

While the market has returned to loving CrowdStrike after a nine-month or so break, I do not believe it’s returned to loving CrowdStrike with any degree of exuberance, as evidenced by the 2%+ FCF/EV yield (using 35% FCF margins) we’re still being offered for a company that could grow sales at 20%+ annualized for the next decade, the data underpinning which I will share with you later in this note.

Before we get into the broad industry analysis that leads me to conclude this, let’s now briefly review CrowdStrike’s exceptional financials.

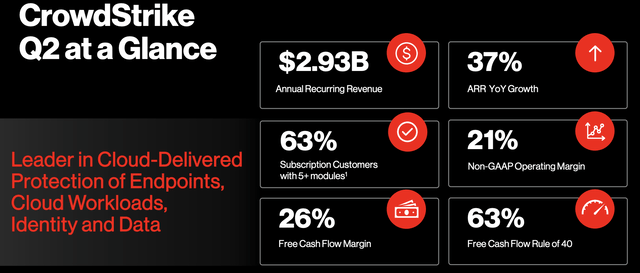

Financial Analysis

Crowdstrike Q2 2023 Earnings Presentation

Unlike some of my younger companies, e.g., Affirm (AFRM), Marqeta (MQ), or Monday (MNDY), CrowdStrike requires far less mental horsepower if you will.

There is no balance sheet that’s written in hieroglyphics as is the case for Affirm (AFRM) (which I, in service to you, understand well, but it’s objectively quite difficult to grasp on some level).

There’s no nuanced understanding of unit economics with which we can predict long-term margin expansion ahead of the broad market. There’s no expectation of future margin expansion.

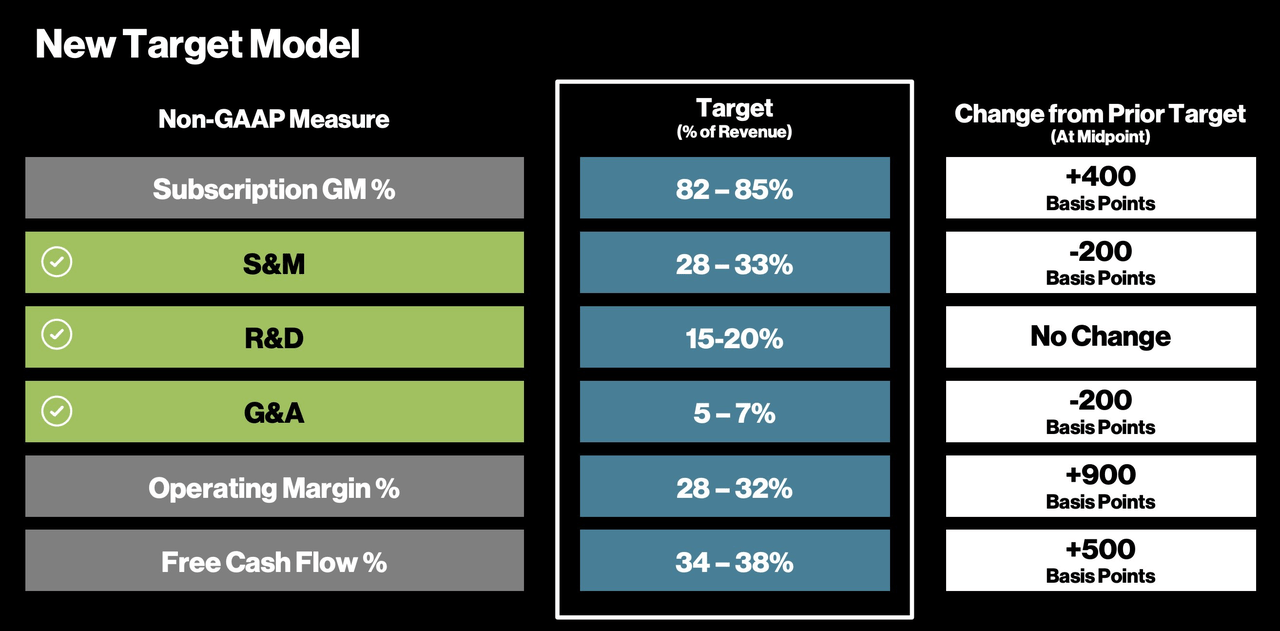

Free cash flow margins are already near their target, fully matured levels.

CrowdStrike’s Long-Term Operating Model (Note 35%+ Free Cash Flow Margin)

We now expect to exit Q4 within our target non-GAAP operating margin model and to remain within our target model on an annual basis starting in FY ’25.

George Kurtz, CEO, Q2 2023 CrowdStrike Earnings Call

Crowdstrike Q2 2023 Earnings Presentation

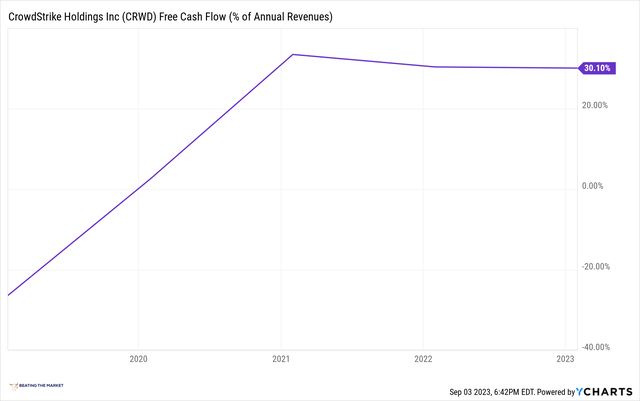

CrowdStrike’s Free Cash Flow Margin Hovers At About 30%, Which Is Near Long-Term Target

YCharts

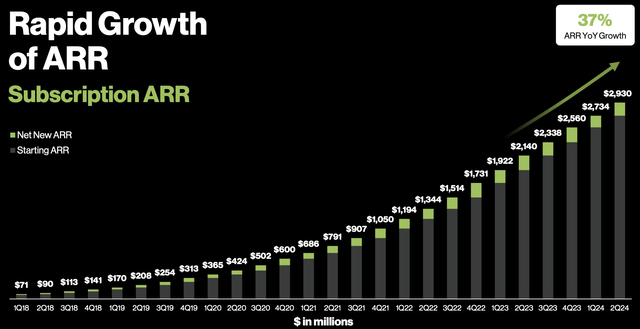

It’s already eclipsed $1B and ARR, and it’s soaring through $3B as I type this.

The business has so much velocity and so many resources in the way of liquid capital and labor capital and brand equity that it would take quite a bit to derail it at this stage.

CrowdStrike’s Breathtaking ARR Growth

We are also observing substantial changes in the competitive landscape, uniquely benefiting CrowdStrike. With the business momentum we see and competitive market dynamics, we believe our second half performance will yield double-digit net new ARR growth.

George Kurtz, CEO, Q2 2023 CrowdStrike Earnings Call

Crowdstrike Q2 2023 Earnings Presentation

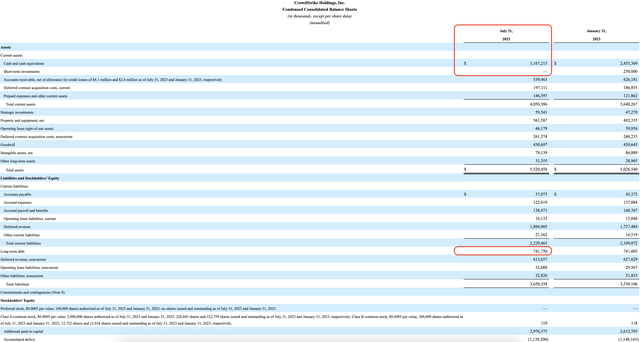

It has ~$3.2B in cash and only ~$750M in long-term debt, to which it adds each quarter via the aforementioned robust free cash flow margins.

CrowdStrike’s Pristine Balance Sheet

CrowdStrike’s 10-Q

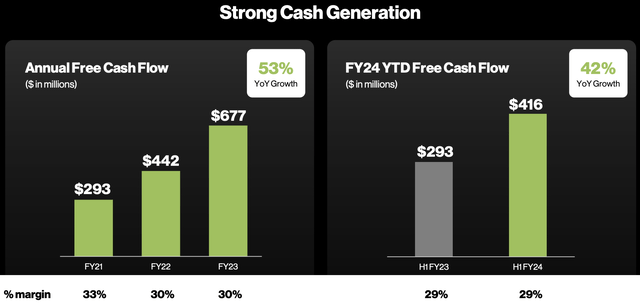

Each quarter it adds to this pristine balance sheet via its robust free cash flow generation, depicted just below.

CrowdStrike’s Free Cash Flow Generation

Crowdstrike Q2 2023 Earnings Presentation

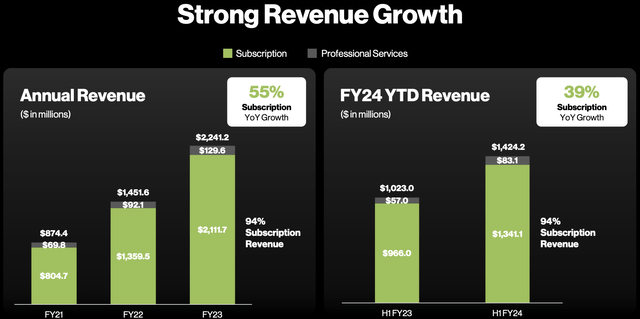

Its business has exceptional embedding/switching costs and network effect moats that make its rapidly growing revenue highly durable.

CrowdStrike’s Rapidly Growing Revenue

Crowdstrike Q2 2023 Earnings Presentation

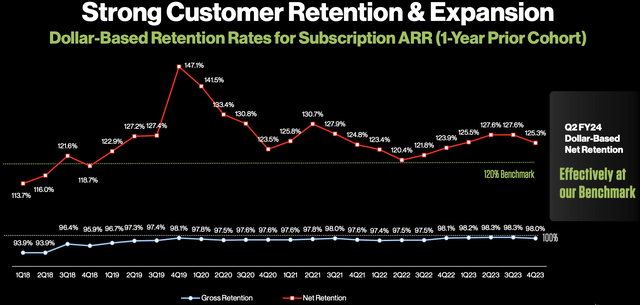

CrowdStrike’s 99th Percentile Net Retention Rate and Gross Retention Rate (Illustrating Embedding Moat)

Crowdstrike Q2 2023 Earnings Presentation

CrowdStrike’s ~99% gross retention rate is a clear indication that the business has a very robust embedding/switching costs moat.

With these ideas as our platform, the final variable that we must assess whereby we develop our long run conviction in the business is the company’s total addressable market, i.e., the long run market opportunity, into which CrowdStrike could grow over time.

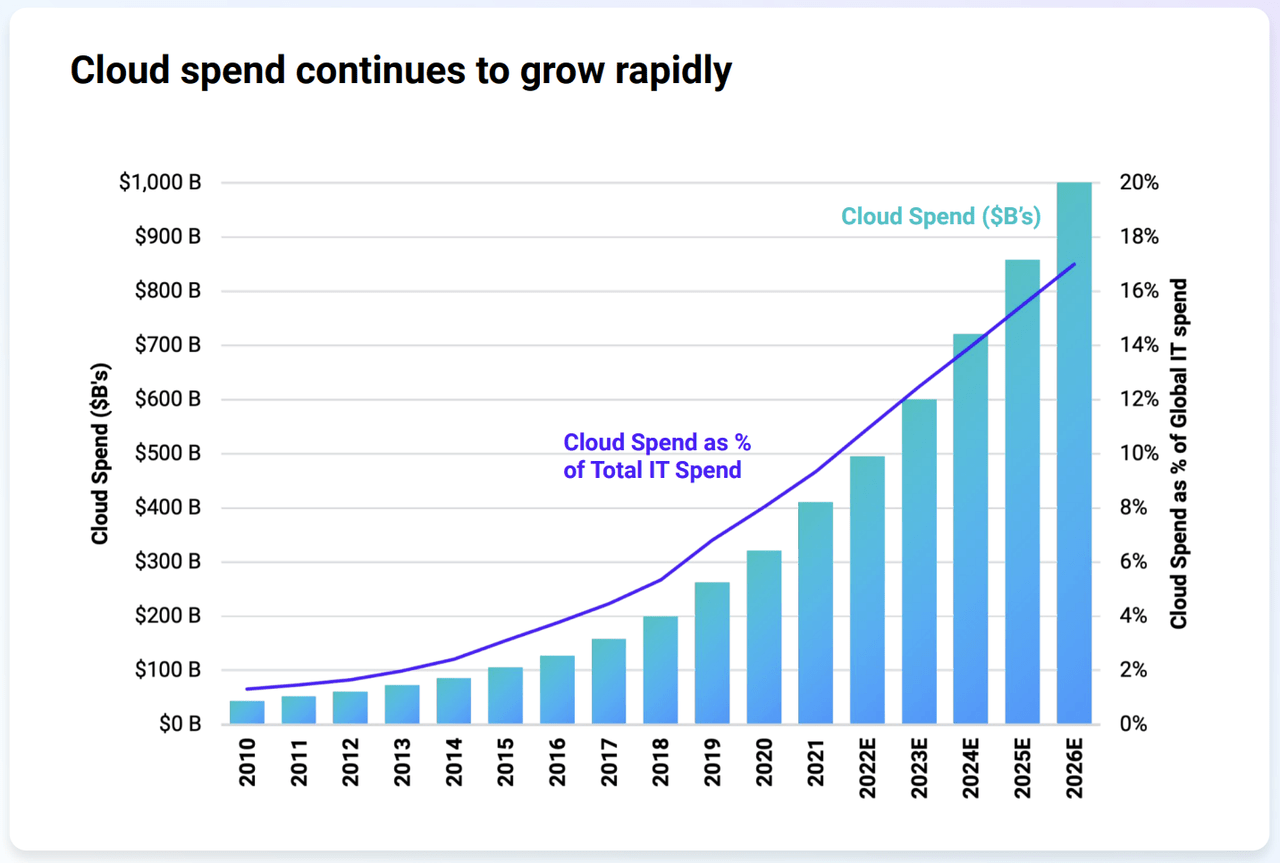

Cloud Computing Is Still Just Getting Started

I’ve shared the following quote often over the last few months, but it certainly bears repeating:

We’ve spent a fair bit of time analyzing what we’re seeing, and I’ve spent a good chunk of time myself looking as well, and we like the fundamentals of what we’re seeing in AWS. The new customer pipeline looks strong. The set of ongoing migrations of workloads to AWS is strong. The product innovation and delivery is rapid and compelling. And people sometimes forget that 90-plus percent of global IT spend is still on-premises. If you believe that equation is going to flip, which we do, it’s going to move to the cloud. And having the cloud infrastructure offering with the broadest functionality by a fair bit, the best securing operational performance and the largest partner ecosystem bodes well for us moving forward.

Andy Jassy, CEO, Amazon Q1 2023 Earnings Call

Datadog (DDOG), which Beating The Market owns from $68/share, recently shared the following chart, depicting the percent of total IT spend globally that has transitioned to the cloud.

The Cloud Is Still Only 10% Of Total IT Spend

Datadog Q2 2023 Earnings Presentation

So we have a very long runway for growth ahead for the cloud computing industry broadly.

But, like the digital ad industry, there are pockets of the cloud computing industry that are growing even more rapidly.

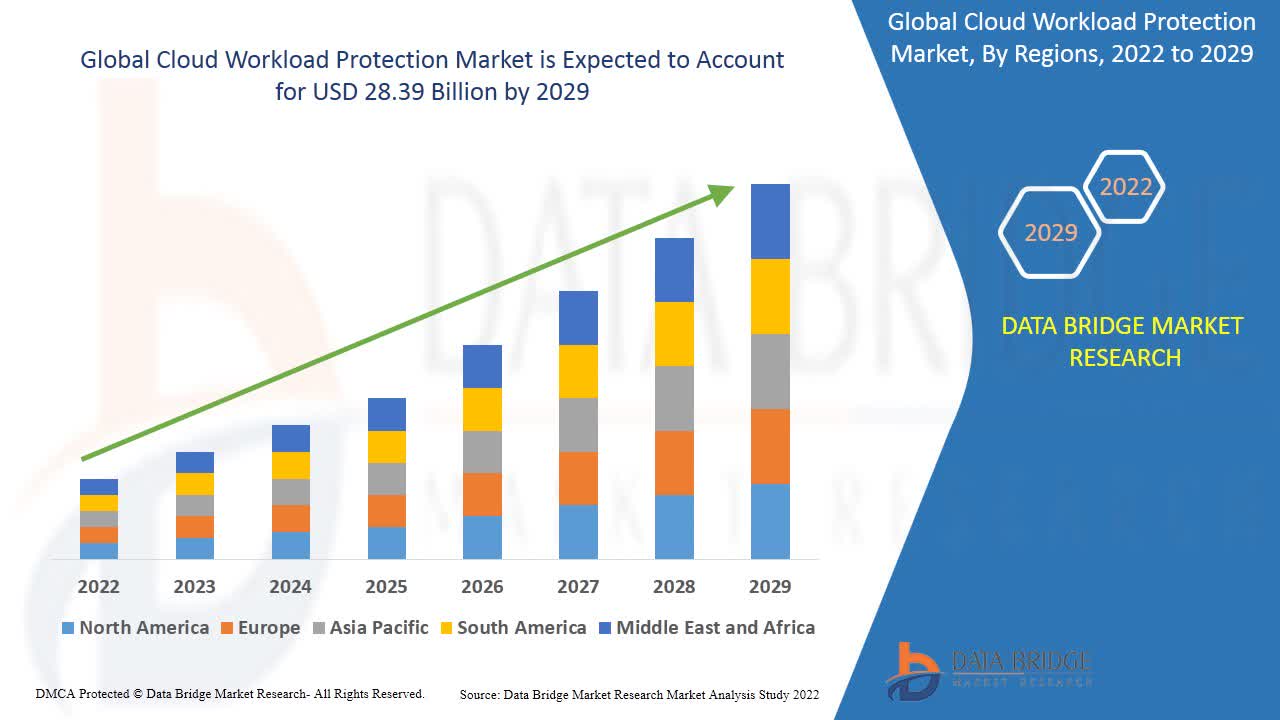

For CrowdStrike,

as well as S1 (S), the Cloud Workload Protection industry, serviced by these companies’ CWPP businesses, is a compelling, rapidly growing subset of the larger cloud computing industry.

The cloud security market opportunity is massive and growing rapidly with the potential to reach $18 billion in calendar year 2026.

[This assertion is substantiated by the cloud workload protection chart shared below, which an independent research shop created.]

Cloud exploitation by adversaries increased 95% year-over-year and the only way to stop threats at all times is with a fully-fledged agent and agentless cloud suite like Falcon. Only CrowdStrike delivers a fully integrated CNAPP solution that unifies cloud workload protection, cloud security posture management, cloud infrastructure entitlement management, threat intelligence and threat hunting in one platform across hybrid and multi-cloud environments. Our leadership in cloud security was recognized in Frost & Sullivan’s recently published 2023 Frost Radar, Cloud Workload Protection Platform report based on our impressive CWPP business growth, our comprehensive cloud visibility and our unrivaled cloud detection and response services.

George Kurtz, CEO, Q2 2023 CrowdStrike Earnings Call

Cloud Workload Protection Market Is Growing Rapidly

Data Bridge Market Research

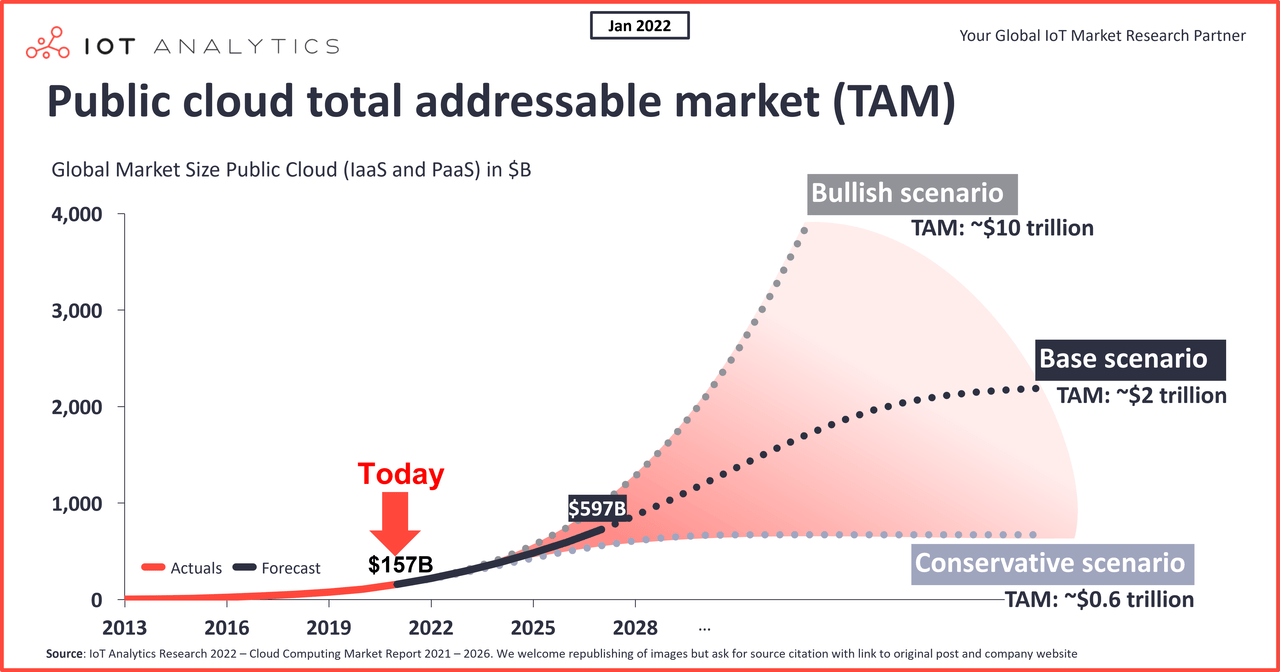

Cloud Workload Protection Market Is A Growing Subset Of The Overall Growing Cloud Computing Market

IOT Analytics

Concluding Thoughts

Despite an incredible rise this year, using 35% free cash flow margins, CrowdStrike remains fairly attractively valued at these levels, and I think the recent somewhat parabolic move represents the market pricing in this new long-term projected margin structure.

With these ideas in mind, let’s turn to a review of CrowdStrike’s current, more nuanced valuation.

| Key Metrics | Values |

| 2023 Net Revenue | ~$3B |

| Long Run Free Cash Flow Margin (low end of guidance) | 35% |

| 2023 Pull Thru Free Cash Flow | ~$1B |

| Shares Outstanding | 242M |

| Net Cash | ~$2.5B |

| Enterprise Value | $43B |

| Free Cash Flow/Enterprise Value Yield | 2.3% |

Considering the business will very likely grow sales at 20%+ sustainably for the next 5-10 years, I believe a 2.3% yield is fairly attractive.

Is it $112/share? Is it $149/share? No, but I still like it here (don’t love it).

Of course, the inverted yield curve indicates that a recession is either already here or imminent, and this could create hiccups in CrowdStrike’s growth rate, which would result in the above valuation not being as attractive as I believe it to be today.

Thank you for reading, and have a great day.

Read the full article here

")

")

2026-04-06")

")

")