")

")

")

Shengfeng Development Limited (NASDAQ:SFWL) recently delivered news about the acquisition of electric heavy-duty trucks and further electrification efforts, which may interest funds focused on ESG efforts. I also believe that further technological development of the Shengfeng Transportation Management System may bring profit margin growth in the coming years. I do see risks from the current equity structure, governmental intervention, and changes in the price of energy. With that, I think that the company appears undervalued.

Shengfeng Development Limited

Shengfeng Development Limited is a Chinese company that provides nationwide contracting and logistics services.

The service package primarily includes traditional logistics services. The company also offers the management of supply capacities for its clients. The company specifically targets clients who do not have little experience of generating business relationships in China in order to accompany and facilitate the insertion of these businesses in the local market as well as the insertion of the products and services.

Shengfeng’s logistics network currently reaches 350 cities within China, and consists of 22 cloud storage centers, 35 distribution centers, 22 service outlets, a total of 600 transportation trucks under its ownership, and 40 thousand transportation providers.

The activities are divided into three operating segments; B2B freight transportation, cloud storage, and value-added services. The first one covers traditional logistics operations of land movements between business and business. The second segment is oriented exclusively to the online data storage solution of its clients and the relevant communication network in this regard. Finally, the last of these segments includes supply chain management and productivity services within its clients’ business structure.

Although the proposal of the storage segment and supply chain management are potentially attractive to expand as an easy-access option in the disembarkation of companies to Chinese territory, it is still the traditional logistics segment that represents the largest amount of income. In any case, storage networks are highly functional for the company in relation to the administration and preparation of transportation schedules, and it is projected that the two segments that currently represent minor percentages of annual revenues may have sustained growth in the short term future.

Balance Sheet

The last balance sheet reported included an asset/liability ratio over 1x, with a current ratio larger than 1x too. I believe that the balance sheet appears solid, and the total amount of long term debt does not appear significant.

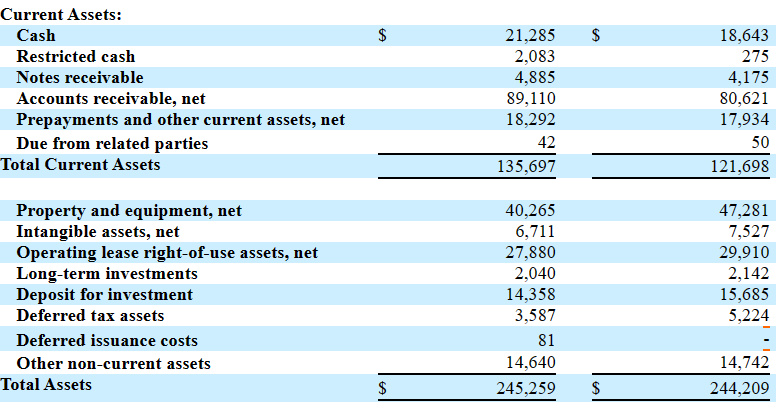

Cash in hand stands at close to $21 million, with accounts receivable close to $89 million, and total current assets of about $135 million. Additionally, with property and equipment close to $40 million and operating leases worth $27 million, total assets are equal to $245 million.

Source: 20-F

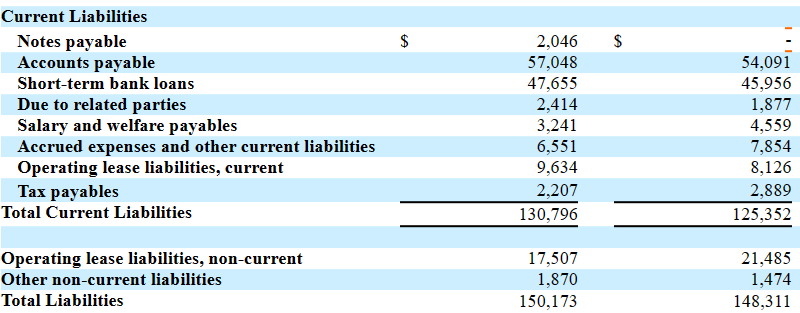

The list of liabilities does not seem scary. Notes payable were equal to $2 million, with accounts payable of $57 million, and short-term bank loans close to $47 million. Besides, total current liabilities were equal to $130 million, with total liabilities of $150 million.

Source: 20-F

I studied a bit the terms of the short-term bank borrowings to understand the most convenient cost of capital in my financial model. The company reported a weighted average interest rate of approximately 4.48% and 4.70% per annum, so I believe that the future WACC would most likely be above these interest rate marks.

As of December 31, 2022 and 2021, the total short-term bank borrowings balance of the Company was approximately $47.7 million and $46.0 million, respectively. The short-term bank loans outstanding as of December 31, 2022 and 2021 carried a weighted average interest rate of approximately 4.48% and 4.70% per annum, respectively. Source: 20-F

FCF Catalysts: Expansion Into New Markets And Expansion Of Its Service Package Will Most Likely Accelerate FCF Margin Growth

In most documents released by management, the strategy seems to be not only a growth strategy, the company also seeks to become one of the leading references within the field of logistics in Chinese territory. Part of this growth is predicted by the expansion into new markets towards the interior of China as well as the penetration of its distribution networks in highly concentrated urban areas around large cities, such as Beijing and Yangtze, as well as in the West of the country. Under my base case scenario, I assumed that these strategies will successfully enhance net sales growth and the net income margin.

Along with this, the expansion of its service package and the strengthening of its distribution networks for the optimization of operations as well as the reduction in margins and general costs are the key points from management. As a result, I believe that the company will most likely experience profit margin increases in the coming years.

Further Technological Development Of The Shengfeng Transportation Management System

The company relies on its own proprietary Shengfeng Transportation Management System. With some cash in hand to design new features, the company would most likely deliver further operating performance thanks to new designs like transportation and tracking management, payment calculation, client services, storage management, and order management. I believe that sufficient new implementations and applications could enhance FCF margins in the coming years.

Further ESG Efforts Like Electrification Or Acquisition Of New Electric Heavy-Duty Trucks Will Most Likely Bring Demand For The Stock

Considering the recent acquisition of Electric Heavy-Duty Trucks and the words from management, I believe that the company is going in the right direction in terms of ESG efforts. In my view, if management continues to make efforts to reduce emissions and utilize more green energy, more funds will most likely have a look at the business model. Let’s keep in mind that there is a significant amount of new funds and investors assessing investments in companies that make efforts in this regard.

Electrification has become mainstream throughout the automotive industry, and Shengfeng will follow the trend by utilizing green energy to reduce logistics costs, while also striving to make contributions to energy conservation, emissions reduction, and environmental protection. Source: Shengfeng Development Limited Purchases Electric Heavy-Duty Trucks

Free Cash Flow Model

For the assessment of future sales growth, I assumed sales growth in both the transportation segment and the warehouse store business segment. I expect that transportation would report net sales close to $414 million in 2024 and $742 million in 2034. Additionally, warehouse storage will most likely provide revenue worth $28 million in 2024 and 2034 net sales close to $67 million. Total sales will most likely go from around 7% in 2024 to close to 5%-14% in 2034.

Source: My DCF Model

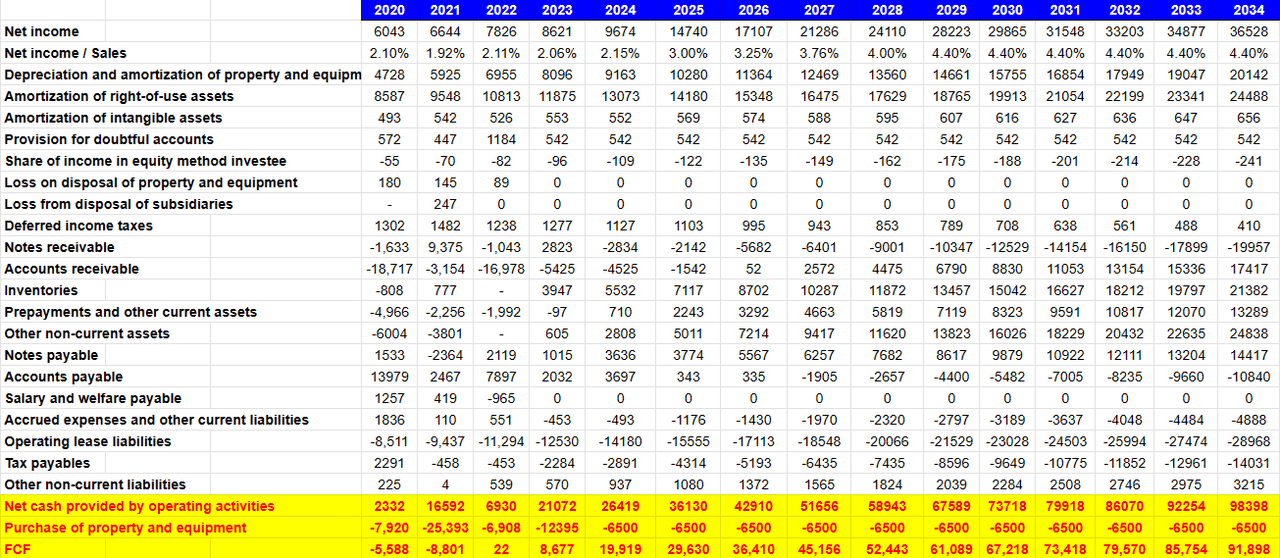

With the previous net sales forecast, I also assumed some increase in the profit margin from around 2% in 2024 to close to 4% in 2034. With the previous assumptions, I obtained 2034 net income of close to $36 million and total net sales of $830 million.

Source: My DCF Model

Also taking into account previous cash flow statements and my previous assumptions, I took into account 2034 depreciation and amortization of property and equipment close to $20 million, with amortization of right-of-use assets worth $24 million. I did not include amortization of intangible assets, provision for doubtful accounts, and loss on disposal of property and equipment, which I believe are extraordinary events.

Besides, with changes in accounts receivable of close to $17 million, changes in inventories worth $21 million, changes in prepayments and other current assets of about $13 million, and changes in notes payable close to $14 million, I obtained accounts payable worth -$11 million. Finally, 2034 net cash provided by operating activities would stand at close to $98 million, and with 2034 purchase of property and equipment of about -$7 million, 2034 FCF is expected to be at around $91 million.

Source: My DCF Model

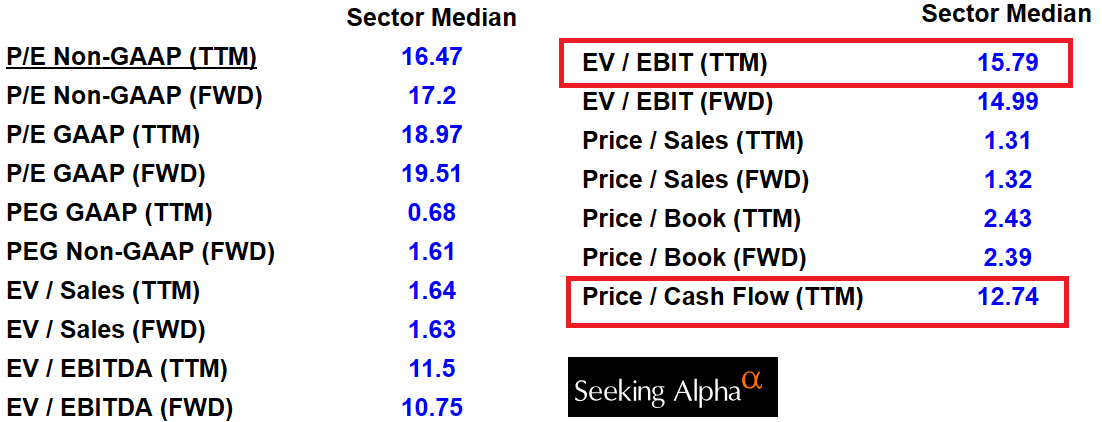

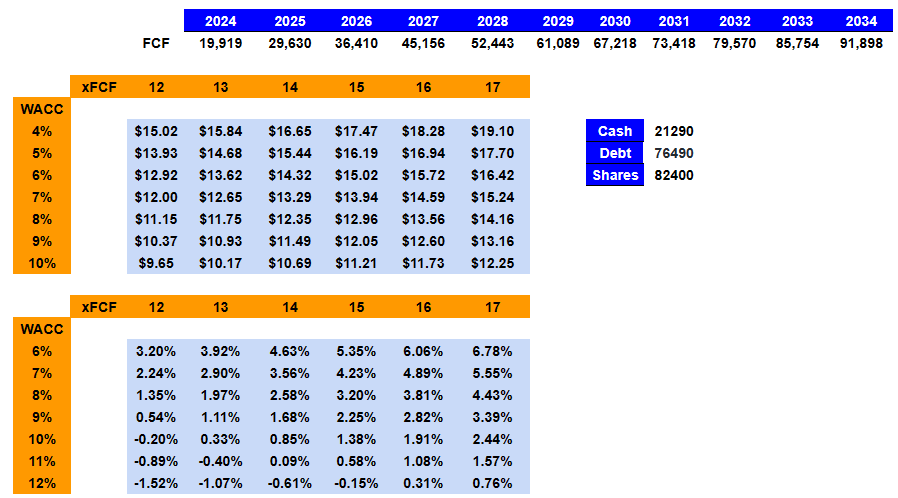

With the previous cash flow statement model, I obtained FCFs close to $29-$91 million from 2024 to 2034. Besides, assuming an EV/FCF of about 12x-17x, cost of capital ranging from 4% to 10%, $21 million in cash, and debt of $76 million, I obtained a target price ranging from $9-$19 per share and a median close to $13.5-$14.5 per share. Notice that I took a look at the valuation of the sector for the assessment of the terminal EV/FCF multiples. The following figures were obtained from the Seeking Alpha platform.

Source: SA

The maximum internal rate of return would be close to 6%. However, in most cases, the internal rate of return remains positive. Hence, I believe that the stock appears a bit undervalued.

Source: My DCF Model

Competitors

The contracted logistics industry in China is highly competitive and very fragmented since there are a large number of regional participants that provide domestic services and a series of large firms, including Sinotrans. Logistics Ltd., Beijing Changjiu Logistics Co., Ltd., and Kerry Logistics Limited make up Shengfeng’s main competitors. The company is confident that its historical establishment as an agent in this industry provides it with significant advantages in the competitive order. It also admits that in the expansion of its services, it will find new participants in this competition.

Risks

A large part of the risks for this company passes exclusively through the intervention of the Chinese government on the trade channels and industrial regulations in each case. This applies to future acquisitions and mergers as well as the internal legislation of each of the subsidiaries of this company. In other words, any such complication from the outsourcing of the service, which includes 30% of the activity of its traditional logistics segment, as well as variations in the price of fuel can generate disruptions in the operating margins of this company.

I also believe that criticism from regulatory agencies, such as the SEC, could push the stock price down as demand for the shares may decline. In this regard, management provided a significant explanation in the last annual report.

U.S. public companies that have substantially all of their operations in China have been the subject of intense scrutiny, criticism, and negative publicity by investors, financial commentators, and regulatory agencies, such as the SEC. Much of the scrutiny, criticism, and negative publicity has centered on financial and accounting irregularities and mistakes, a lack of effective internal controls over financial accounting, inadequate corporate governance policies or a lack of adherence thereto and, in many cases, allegations of fraud. As a result of the scrutiny, criticism, and negative publicity, the publicly traded stock of many U.S. listed Chinese companies sharply decreased in value and, in some cases, has become virtually worthless. Source: 20-F

Conclusion

Shengfeng Development Limited continues to deliver net sales growth, and may report FCF growth thanks to expansion into new markets towards the interior of China and new distribution networks. I also believe that the recent acquisition of electric heavy-duty trucks and electrification plans announced by management may bring the attention of investors interested in ESG investments. Finally, further technological development of the Shengfeng Transportation Management System will most likely bring operating efficiency and profit margin growth. There are obvious risks from the current equity structure, governmental intervention, or changes in the price of crude oil. With that, I believe that the company trades a bit undervalued right now.

Read the full article here

")

")

2026-04-06")

")

")