")

")

")

The pre-market is looking difficult for Sapiens International (NASDAQ:SPNS) due to its associations with Formula Systems (FORTY), an Israeli holding company which controls SPNS, in a moment where Israel is under attack and has declared itself in a state of war. While other Formula Systems companies are under more uncertainty from a business perspective due to their exposure in large proportions to Israeli demand, SPNS only has 10% exposure to Israel, which limits their uncertainty and probably means the pre-market panic is overdone. The declines in pre-market seem to be in the sizes where they imply Israeli revenues are permanently crippled by being proportional to the total Israeli exposure. The reality is that Israel, despite violence towards its civilian citizens, will probably see somewhat normalized business activity quite soon unless a very alarming escalation occurs, which at that point would become more systemic due to its possible effects on longer-term oil prices and the complexity that would be introduced to America’s job to take action now and help guarantee the safety of civilians as well as manage the tensions with other neighboring countries whose relations with Israel have been very poor historically.

While it is not responsible to comment extensively on the news developments as the story continues to unfold, it is clear that there is still a lot of entropy and a range of possibilities from this point, from some de-escalation or limits to belligerents in this new conflict, to severe escalation, all remain possible. But the key takeaway as far as SPNS is concerned is that the magnitude of exposure to Israel at this uncertain time is very limited, and that on the volatility likely to be experienced by SPNS at open and throughout the day, is likely to be a buying opportunity when the volatility is to the downside. However, we still believe even at a daily bottom, the PE is a little high on SPNS compared to benchmark rates.

SPNS Case Before Today

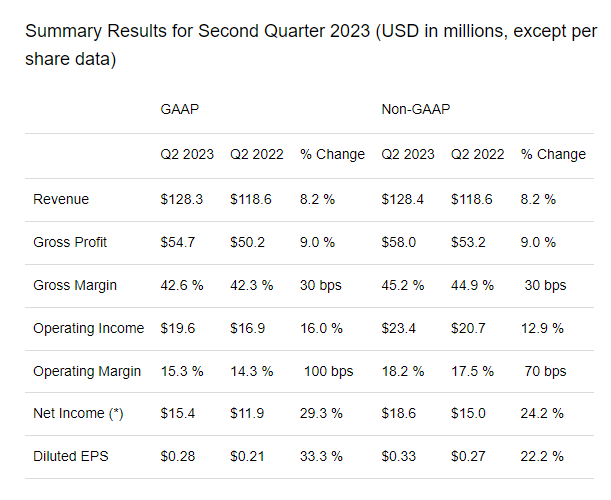

The case before today was quite compelling for SPNS. They are an insurtech company, and they are achieving strong sales growth and even stronger profit growth. Fixed cost increases were limited, and the only line that matched the growth of sales was R&D as they try to implement NLP tools from OpenAI, in lieu of their recently announced partnership with Microsoft (MSFT) that will look to apply these technologies to the insurance industry around documents like policies and such for customers.

Sales grew by 8.2% including currency headwinds. North America matched the average growth of the company, while Europe lagged at 5.2%. APAC growth, a newer geography representing about 10% of revenue, grew by 25% lead by new signings with national insurance players in first line insurance in ASEAN countries primarily. All products were selling well, including reinsurance as well as the more attractive P&C and Life markets, which expose SPNS to higher quality clients. Operating profit grew by 16%, and net income by 30%.

Q2 IS (Q2 2023 PR)

SPNS began reporting on a new segment basis, which boils down to an integration segment versus a recurring software revenue segment. Moreover, SPNS is undergoing shifting customers to a cloud-based suite of its software. The recurring revenues have a gross margin of 54.8%, where the average margin is 42%, so vaguely speaking, the integration revenues that involve implementing the software for customers, time for doing so being billable, makes a little over 30% in gross margin, or almost half of the recurring segment. Since naturally customers that were paying for integration become onboarded and then pay for service, there is a margin uplift on the cash streams coming from customers, and the integration versus the recurring gross margin is around a 5:8 ratio. SPNS thinks it will graduate to 1:3 in a couple of years as the base of customers on the recurring cash streams grows. Margin could go up 5% if thing pan out.

Bottom Line

Revenue growth accelerated, meaning customer apprehension has dissipated to our surprise, reinforcing the notion that the US economy is doing pretty well after all. The <10% exposure to Israel, while likely to experience some period of disruption in business development, will likely continue to generate recurring cash and will not be impaired. While the conflict in Israel could develop a lot further, prompt declarations by Iran to distance themselves from the planning of this specific attack shows avenues in which the casus belli for further escalation beyond Israel’s borders could be limited, which means limited market impact. The biggest risk to markets right now is the involvement of more belligerents in this conflict, specifically Iran, with echoes of 70s embargoes of oil likely still fresh in many allocators’ minds when major oil producing nations acted during Israel’s wars to keep its country.

A risk to SPNS is that it does escalate, at which point global markets would see a more severe sell-off as oil supplies would likely be impacted, contributing to general inflationary fears that are intrinsic to higher-conflict periods in history.

Pre-market showed readings around 6% of declines, and the open could be very volatile. We believe that on the increment, this presents a buying opportunity. However, despite the strong SPNS performance, we believe that even if discounted on today’s market and at points in trading during the day, the SPNS multiple is a little high at 24x PE on the basis of just their already existing insurtech end-markets, being somewhat second-tier, in the context of higher benchmark rates. While the growth allows for lower earnings yields than the risk-free rate, and the growth was quite the overperformance given the talk about slower sales velocity this year, the price is just not especially compelling.

Read the full article here

")

")

2026-04-06")

")

")