(NASDAQ:PANW)")

")

A Quick Take On Guardian Pharmacy Services

Guardian Pharmacy Services, Inc. (GRDN) has filed to raise $115 million in an IPO of its Class A common stock, according to an SEC S-1 registration statement.

The firm provides pharmacy services to patients in a variety of assisted living environments.

Guardian Pharmacy Services, Inc. has produced steadily growing revenue and profits in recent years.

I’ll provide a final opinion when we learn more IPO details.

Guardian Overview

Atlanta, Georgia-based Guardian Pharmacy Services, Inc. was founded to assist patients living in assisted living, behavioral health and long-term healthcare facilities with their pharmaceutical requirements.

Management is headed by co-founder, President and CEO Fred Burke, who has been with the firm since its inception and was previously co-founder and president of Central Pharmacy Services and Sales Technologies, both of which were later acquired.

The company’s primary focus is on the following facility types:

-

Assisted living facilities

-

Behavioral health facilities

-

Skilled nursing facilities.

The firm provides services to patients to help them optimize their pharmacy benefit plan coverage, analyzes potential adverse drug interactions, provides customized compliance solutions and integrates with the facility’s electronic medication administration records system.

As of June 30, 2023, Guardian has booked fair market value investment of $76.8 million from investors, including Bindley Capital Partners, Cardinal Equity Fund and Pharmacy Investors.

Guardian Customer Acquisition

The firm pursues clients operating networks of long-term care facilities that seek Guardian’s combination of billing solutions, clinical support and pharmacy adoption services.

As of June 30, 2023, the company operated 43 pharmacies serving 156,000 patients in approximately 5,800 long-term care facilities in 28 states.

Selling, G&A expenses as a percentage of total revenue have varied within a narrow range as revenues have increased, as the figures below indicate:

|

Selling, G&A |

Expenses vs. Revenue |

|

Period |

Percentage |

|

Six Mos. Ended June 30, 2023 |

14.7% |

|

2022 |

15.1% |

|

2021 |

14.9% |

(Source – SEC.)

The Selling, G&A efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Selling, G&A expense, has been stable at 0.9x in the most recent reporting period, as shown in the table below:

|

Selling, G&A |

Efficiency Rate |

|

Period |

Multiple |

|

Six Mos. Ended June 30, 2023 |

0.9 |

|

2022 |

0.9 |

(Source – SEC.)

Guardian’s Market & Competition

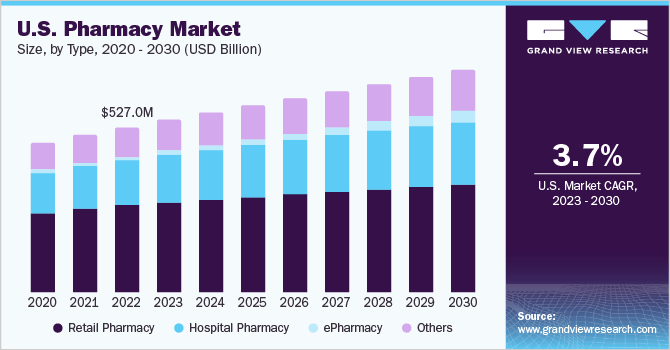

According to a 2021 market research report by Grand View Research, the global market for pharmacy products and services was an estimated $1 trillion in 2020 and is forecasted to reach $1.4 trillion by 2028.

This represents a forecast CAGR (Compound Annual Growth Rate) of 4.3% from 2021 to 2028.

The main drivers for this expected growth are an increasing number of persons requiring medication and related services as the global population ages.

Also, the chart below shows the historical and projected future growth of the U.S. pharmacy products and services market through 2030:

U.S. Pharmacy Market (Grand View Research)

Major competitive or other industry participants include the following:

-

Omnicare

-

PharMerica

-

Remedi SeniorCare

-

Pharmscript

-

PharmCareUSA

-

Polaris Pharmacy Services.

Guardian Pharmacy Services, Inc. Financial Performance

The company’s recent financial results can be summarized as follows:

-

Growing top line revenue

-

Increasing gross profit and stable gross margin

-

Growing operating profit

-

Variable cash flow from operations.

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

Six Mos. Ended June 30, 2023 |

$ 502,385,000 |

15.5% |

|

2022 |

$ 908,909,000 |

14.8% |

|

2021 |

$ 792,072,000 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

Six Mos. Ended June 30, 2023 |

$ 101,540,000 |

15.0% |

|

2022 |

$ 185,866,000 |

15.3% |

|

2021 |

$ 161,265,000 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

% Variance vs. Prior |

|

Six Mos. Ended June 30, 2023 |

20.21% |

-0.1% |

|

2022 |

20.45% |

0.4% |

|

2021 |

20.36% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

Six Mos. Ended June 30, 2023 |

$ 31,752,000 |

6.3% |

|

2022 |

$ 51,990,000 |

5.7% |

|

2021 |

$ 30,150,000 |

3.8% |

|

Net Income (Loss) |

||

|

Period |

Net Income (Loss) |

Net Margin |

|

Six Mos. Ended June 30, 2023 |

$ 30,156,000 |

6.0% |

|

2022 |

$ 49,661,000 |

5.5% |

|

2021 |

$ 28,326,000 |

3.6% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

Six Mos. Ended June 30, 2023 |

$ 41,454,000 |

|

|

2022 |

$ 48,522,000 |

|

|

2021 |

$ 58,498,000 |

|

|

(Glossary Of Terms.) |

(Source – SEC.)

As of June 30, 2023, Guardian had $669,000 in cash and $188.5 million in total liabilities.

Free cash flow during the twelve months ending June 30, 2023, was $45.4 million.

Guardian Pharmacy Services, Inc. IPO Details

Guardian intends to raise $115 million in gross proceeds from an IPO of its Class A common stock, although the final figure may vary.

No existing shareholders have indicated an interest in purchasing shares at the IPO price.

Class A and Class B shareholders will each have one vote per share.

Immediately post-IPO, the company will be considered a “controlled company” by NYSE’s rules.

Management says it will use the net proceeds from the IPO as follows:

In connection with the Corporate Reorganization, each outstanding Common Unit of Guardian Pharmacy, LLC will be converted into [i] one share of Class B common stock of Guardian Inc. and [ii] the right to receive [an as-yet undisclosed amount] in cash (without interest), which we collectively refer to as the Merger Consideration. See “Corporate Reorganization.” We intend to use [an as-yet undisclosed amount] of the net proceeds from this offering to fund the aggregate cash portion of the Merger Consideration. We intend to use the balance of the net proceeds for general corporate purposes and working capital.

(Source – SEC.)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, one of the firm’s subsidiaries is subject to a ‘False Claims Act’ claim, and management declined to quantify the potential liability for the subsidiary.

The listed bookrunners of the IPO are Raymond James, Stephens and Truist Securities.

Commentary About Guardian’s IPO

GRDN is seeking U.S. public capital market investment to fund its merger with the underlying operating entity and for its working capital requirements.

The company’s financials have produced increasing top line revenue, higher gross profit and stable gross margin, growing operating profit and fluctuating cash flow from operations.

Free cash flow for the twelve months ending June 30, 2023, was an impressive $45.4 million.

Selling, G&A expenses as a percentage of total revenue have varied within a narrow range as revenue has increased; its Selling, G&A efficiency multiple was flat at 0.9x in the most recent reporting period.

The firm currently plans to pay no dividends, and any future dividend payments will be at the discretion of the Board of Directors.

GRDN’s recent capital spending history indicates it has spent moderately on capital expenditures as a percentage of its operating cash flow.

The market opportunity for providing pharmacy services to long-term care facilities in the United States is large and expected to grow as the number of Americans living in these facilities increases dramatically.

When we learn more about the IPO’s pricing and valuation assumptions and other terms, including the merger consideration, I’ll provide a final opinion on Guardian Pharmacy Services, Inc.

Expected IPO Pricing Date: To be announced.

Read the full article here

(NASDAQ:PANW)")

")

")

")

2026-04-06")

")

")