")

September 30th marked the end the fiscal year for the U.S. Government.

It also marked that the Federal Reserve has recorded an operating loss of $103 billion for the past 12 months.

Every week over the past year, the Fed has lost money because the interest it is paying on its variable rate liabilities, namely its $ 4.9 trillion in bank reserves and reverse repurchase agreements, exceeds the interest income it is earning on its $7.7 trillion fixed rate System Open Market Account (SOMA), comprised mainly of U.S. Treasury and Mortgage-Backed Securities.

The losses have grown as the Fed has raised rates to fight inflation.

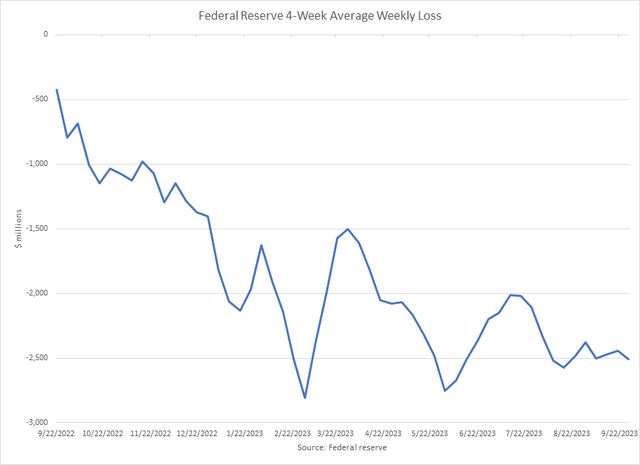

Federal reserve

Currently the Fed is losing, on average, $2.5 billion per week.

Why The Fed Is Losing Money

As we’ve written about previously here, the Fed is losing money because its balance sheet has what is called an Asset/Liability mismatch. The assets on the balance sheet in the SOMA portfolio have long-term maturities and earn a fixed rate, yielding approximately 2.0%. On the liability side of the balance sheet, the Fed pays a variable rate on its short-term bank reserves and reverse repurchase agreements. This Asset/Liability mismatch exposes the Fed to interest rate risk if rates go up.

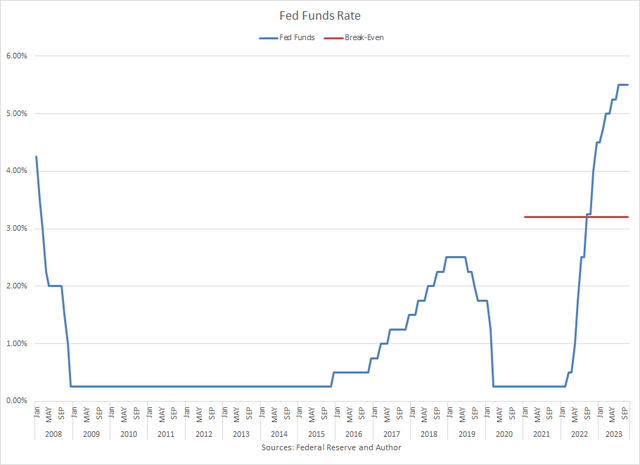

The variable rate for the liabilities is tied to the Fed Funds rate and has moved higher as the Fed has tightened by raising the Fed Funds rate.

Since March, 2022, the Fed has hiked rates at 11 out of the 13 FOMC meetings, for a total increase of 525 basis points, to the new range of 5.25% to 5.50%.

Federal reserve and Author

Currently, the Fed is paying roughly 5.33% on its variable rate liabilities.

The Fed will continue to lose money until the cost of its liabilities drops below the break-even rate, which we estimate to be 3.2%.

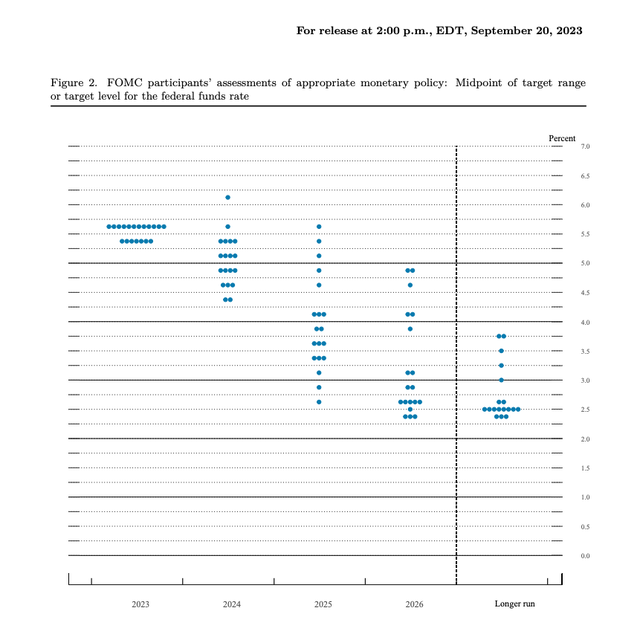

Following the September FOMC meeting the Fed released their updated Summary of Economic Projections (SEP). The SEP represents each participant’s projections based on information available at the time of the meeting.

While the Fed kept rates unchanged in September, their updated SEP suggests that the Fed will hold interest rates at the historically high levels for longer than previously anticipated. They are still looking for one more rate hike in 2023, but the expectation is now that rates will be at 5.1% by the end of 2024, up from June’s projection of 4.6%. While previously the SEP was looking for (at) 100 basis points in rate cuts in 2024, it is now projecting only 50 basis points in cuts next year.

Federal reserve

According to the SEP, FOMC participants don’t anticipate rates declining below the 3.2% breakeven rate until 2026.

If so, the Fed will lose money for at least another three years. By then, the cumulative operating loss could exceed $300 billion.

Fed to Cut Payroll

Unlike many other government agencies, the Fed does not come under the control of congress and its budget is not a part of federal spending. Instead, it is a self-funding institution.

Since inception, the Fed has earned money through what is called “seigniorage,” whereby they make money by creating money. Seigniorage refers to the interest a central bank earns on creating money less the cost of producing, distributing and replacing currency, or bank notes. These earnings are used to cover the operating costs of the central bank. It is a way for a central bank to earn a profit to be self-sustaining.

By statute, all earnings in excess of expenses are returned to the US Treasury. The Treasury uses this distribution from the Fed as a source of revenue to reduce its fiscal deficit.

In 2023, however, for the first time ever, due to its operating losses, the Fed will not have the seigniorage, or income, to cover its overhead. Additionally, there will be no distribution to the Treasury. Instead, it will create new reserves to meet these obligations.

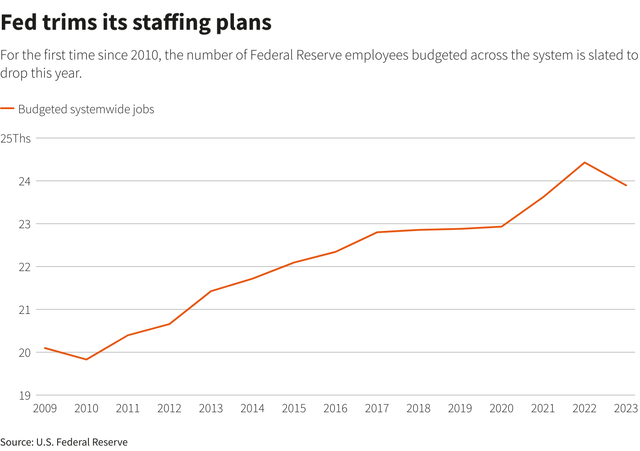

As a result, the Fed is being mindful of its operating expenses. In this vein, for or the first time in 13 years, the Fed is reducing its headcount.

Reuters reported here that the Fed will be cutting its employment rolls by 300 this year. The eliminated positions will come from a combination of early retirements, not filling openings due to attrition, and layoffs.

Federal Reserve

We may see more signs of belt tightening in the future.

Higher for Longer Interest Rates

In addition to short rates rising due to the Fed rate hikes, longer interest rates have also been moving higher. While many investors have been anticipating a Fed pivot, which is a cut in rates, for quite a while, in some cases since July of 2022, it seems that they have, for now, thrown in the towel.

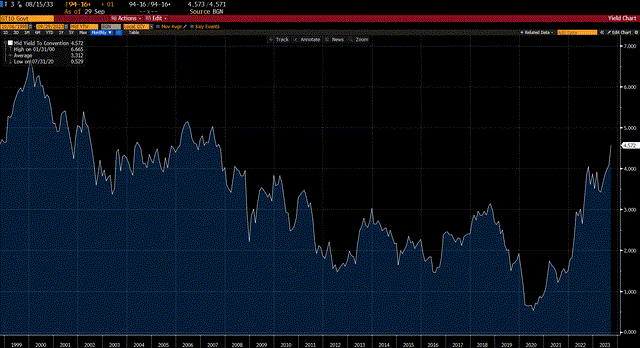

This past week the yield on the 10-year Treasury Note rose to 4.65%, its highest level in 16 years, before settling a bit at quarter end.

Bloomberg

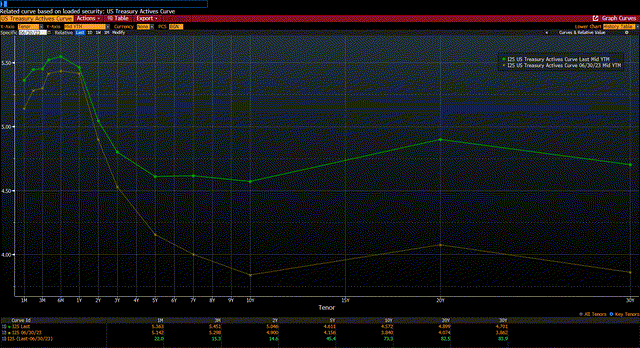

The entire yield curve has actually flattened as long rates have risen, trying to catching up to short rates, as investors are finally accepting the Fed’s “higher for longer” mantra with regard to rates.

This can be seen in the following yield curve chart, showing the change in the shape of the US Treasury yield curve from June 30, 2023 to September 30, 2023.

Bloomberg

Between the end of 2Q23 and the end of 3Q23, the yield on the ten-year T-note jumped by 73 basis points to 4.57%. Long rates rose even more with the 30-year T-bond climbing by 84 basis points to 4.70%.

Short rates, meanwhile only rose 15 basis points, causing the yield curve to flatten, or become less inverted.

Unrealized Bond Losses Grow

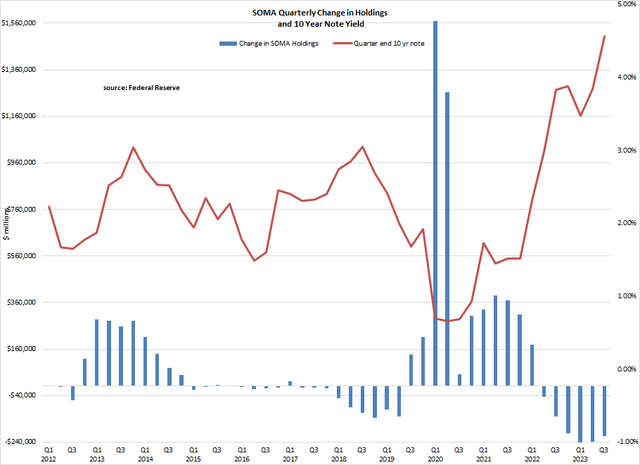

The Fed’s SOMA portfolio consists mainly of long-term US Treasury Securities and Mortgage-Backed Securities. These securities were bought when interest rates were much lower. As can be seen in the chart below, the bulk of the SOMA portfolio was purchased when the 10-year Treasury Note was yielding between 0.50%-2.00%.

Federal Reserve

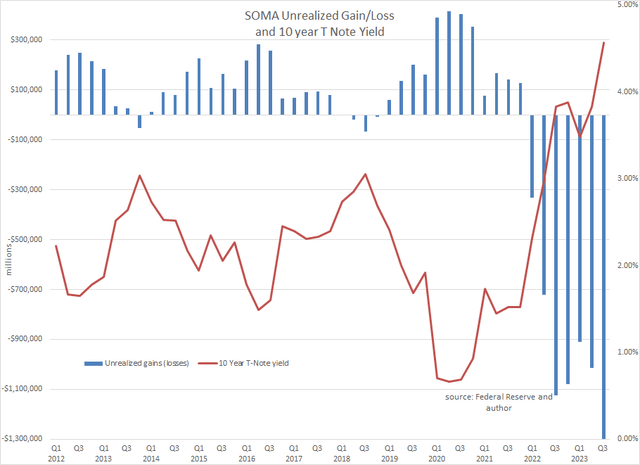

Now that the 10-year Treasury note (US10Y) is yielding 4.57%, the market value of the entire portfolio is significantly below its cost.

We estimate that the loss of the SOMA portfolio has grown to -$1.3 trillion as of the September 30, 2023 quarter end.

Federal reserve and Author

Fortunately for the Fed, they use an amortized cost accounting method, as approved by the Fed Board of Governors, so that their financial statements don’t have to recognize the decline in market value. The losses on the SOMA portfolio are unrealized. Instead, they are only reflected in a footnote on the Fed’s financial reports.

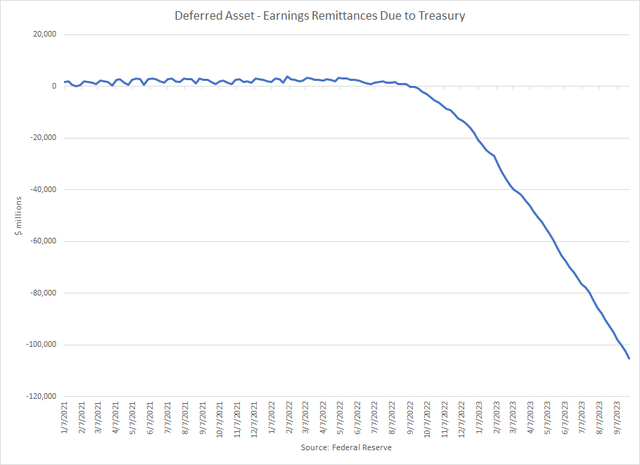

Deferred Asset

Under the Fed’s accounting policy, their operating losses are recorded in a deferred asset account called “Earnings Remittances Due to Treasury” as a negative liability on their balance sheet. They therefore, are able to protect their capital account, as the losses have no accounting effect on the Fed’s capital.

This is fortunate, as their cumulative losses total $105 billion, while the Fed’s capital is only $42 billion.

Federal Reserve

The expected future losses will cause the deferred asset account to grow. When earnings turn positive, they will be used to reduce the deferred asset account before the Fed resumes its remittances to the Treasury.

It is estimated that the deferred asset account won’t be eliminated until 2030, at the earliest. As such, the Fed will not be distributing earnings to the Treasury for quite some time. This revenue shortfall must be replaced by the Treasury, and the cost will ultimately be borne by the taxpayer.

Implications

The Fed’s operating losses and unrealized SOMA losses are large and growing.

The fact that the Fed uses favorable accounting treatment to hide the severity of the losses does not mean that they have not caused significant financial deterioration to the Fed.

The Fed states that “While the rising interest rates have ancillary effects for the Federal Reserve’s income and the unrealized position of the SOMA portfolio, none of these effects impair the Fed’s ability to conduct monetary policy or to fulfill an of its other responsibilities.”

While this may be true in the short run, the longer-term impact is not clear.

The financial deterioration could affect the Fed by limiting its flexibility in implementing policy. This can manifest itself in three ways. The first is by losing its independence. There is already pressure on the Fed from congress, and signs of financial weakness, including widespread discussion of its losses, may result in efforts to put more congressional oversight on the Fed. The second area of concern is market confidence. In many ways, the stability of our financial system is due to the confidence that the central bank is stable and in control. Continued financial weakness may erode that confidence. The final area of concern is more practical. As losses continue to mount and the Fed is forced to create more reserves to meet their obligations, they would be implementing actions that are inflationary and in direct conflict with executing their mandate for stable prices.

Despite the Fed’s reassuring statements, the Fed’s financial health is the weakest it’s been in its history. This is not a place the world’s most important central bank wants to be.

Read the full article here

")

(NASDAQ:PANW)")

")

")

")

2026-04-06")

")

")