")

")

Investment action

Based on my current outlook and analysis of Palo Alto Networks (NASDAQ:PANW), I recommend a buy rating. I believe the secular uptrend for demand for cybersecurity solutions will remain in the uptrend for the coming decade, especially as cyberthreat continues to evolve. PANW’s efficient R&D strategy should continue to ensure that its product offerings stay relevant.

Basic Information

PANW provides network security solutions. The company’s solution offerings spread across network security, cloud-native application protection, security operations, and endpoint security and are available across multiple key industries.

PANW

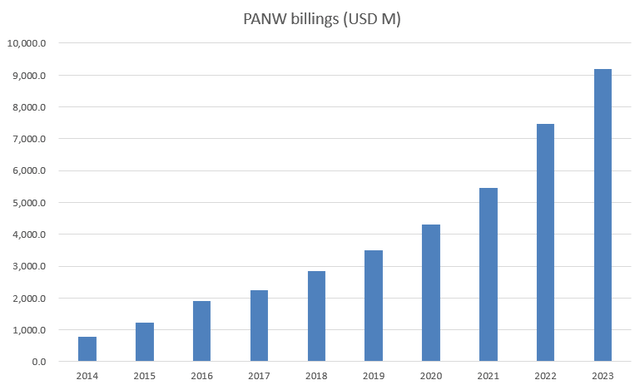

Through the years, PANW as a business has continued to benefit from digitalization, which has increased the need for cyber security. This can be seen clearly from PANW’s historical performance, where billings (calculated by adding the change in deferred revenue to revenue) have consistently climbed every year for the past 10 years. While COVID might have impacted many businesses, PANW saw no signs of a slowdown. In fact, I believe the happening of COVID was a tailwind to PANW as companies were forced to adopt digital tools for remote work purposes. That also leads to more demand for cybersecurity solutions.

Author’s work

Review

Billings growth momentum continued into 4Q23, coming in at $3.16 billion, with total revenue up 26% vs. last year, which is an acceleration from 3Q23, which saw 24% y/y growth. The adjusted EBITDA performance was similarly robust, totaling $693 million (a margin of 29.8%). I take the fact that management is projecting billings to increase by 19.1% year over year by FY24’s midpoint as a very positive indicator of the state of demand that the company is currently experiencing. Notably, the 19.1% implied growth is an acceleration from the 17.7% y/y seen in 4Q23, implying some sort of recovery.

A key concern regarding PANW is the short-term outlook. Remember that PANW sells its product offerings mainly to large enterprises, and many of these enterprises are scrutinizing deals given the rising cost of capital (due to the rising rates). However, in my opinion, cybersecurity is an absolute must for many modern businesses. Companies are not likely to completely forego adopting cybersecurity solutions to save a few million dollars now but end up spending much more in the long run. As the economy recovers, I believe growth rates will return to normal. Importantly, management has noted that growth has returned to more normalized levels in hardware as a result of improved supply and customers digesting prior orders, suggesting that demand is beginning to recover.

We did see however, see two impacts on the top line from the changing environment. First, the rising cost of money has caused customers to hold onto their cash, and more frequently seek deferred payments — payment terms. 4Q23 call

I believe the future is bright for PANW. Growth momentum should continue for as long as cybersecurity is a major theme within enterprises and PANW continues to innovate. For the former, I urge readers to read this article by the World Economic Forum that articulates the seven key trends that will drive demand for cybersecurity in the future. While it is impossible to virtually quantify the exact TAM, a survey done by McKinsey last year suggests that there is a $2 trillion market opportunity for cybersecurity technology and service providers to capture. In short, this is a massive market, and I expect PANW to continue capturing share if they can constantly innovate.

In terms of positioning the company to take advantage of the ongoing long-term trend, I think PANW has a highly efficient and successful research and development (R&D) strategy. During the 4Q23 call, the management emphasized PANW’s commitment to organic R&D and mergers and acquisitions (M&A). They highlighted that the company evaluates 250 private firms each year, giving top priority to M&A when allocating capital. It’s crucial to remember that active adversaries, aiming to undermine the foundations of these products, pose a significant challenge in the field of security. Consequently, the R&D process has shifted from gradual improvements to more revolutionary innovations. Businesses can no longer rely solely on producing faster and better product iterations to counter ever-evolving threat vectors. Therefore, I believe that M&A, particularly the acquisition of early-stage, cutting-edge security firms, represents one of the most effective ways to strengthen competitive advantages. This approach simplifies the integration of acquired technology and teams, while also leveraging revenue synergies by introducing new products to the existing customer base through a more robust go-to-market strategy.

Valuation

Author’s work

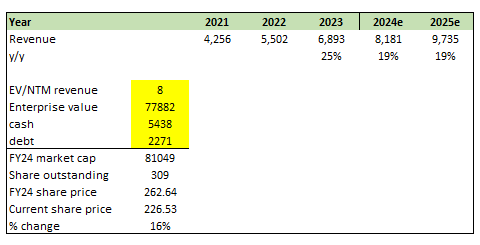

I believe PANW can grow at 19% for the next 2 years. This 19% expected growth is anchored against management FY24 billing guidance for 19%, which I believe is entirely possible given that growth seems to be normalizing, the cyber security uptrend remains strong, and management R&D strategy allows them to roll out or reiterate solutions to meet new threats very efficiently. With my expected growth and PANW relative in-line performance vs. peers on all key metrics (growth, margins, revenue size, leverage ratio), I believe the market will continue to value PANW at 8x NTM revenue. With my assumptions, my price target for PANW is $260, 16% upside from the current share price of $226.

Author’s work

Risk and final thoughts

The risk in dealing with cybersecurity is that things are moving very rapidly. The solution used to address a threat today might be useless tomorrow. While I admire and am positive regarding PANW, there is no guarantee that it will be able to fully address all cybersecurity solutions, especially at the rate at which these cyber threats are evolving. Failure to do so could be fatal to business growth.

My final thought is to recommend a buy rating for PANW based on my analysis. The company is well-positioned to capitalize on the strong secular uptrend in cybersecurity, supported by its efficient R&D strategy. Recent results show billings growth momentum, strong revenue performance, and positive EBITDA figures. While short-term concerns exist due to cautious enterprise spending, the necessity of cybersecurity solutions remains intact. PANW’s long-term outlook is promising, given the ongoing cybersecurity trends and a potential $2 trillion market opportunity.

Read the full article here

")

")

(NASDAQ:PANW)")

")

")

")

2026-04-06")

")